(Subscribers got this to their email January 12. Subscribe to Oz Buzz if you would like to see it sooner.)

January 15, 2022

“The factory of the future will have only two employees, a man, and a dog. The man will be there to feed the dog. The dog will be there to keep the man from touching the equipment.” –Warren G. Bennis

WATCH VIDEOS:

Oz Buzz 66 summary will be on youtube.com shortly

youtube.com/jurockvideo

Also: We will send out a NEW SURVEY next week.

We ask that you please take a minute to vote on the various options that face Oz Buzz and help us decide. Oh, and the first 10 responders will win (pick up) one of Ozzie’s (older) books.

INTERNATIONAL

- INFLATION

- US AND CANADA INTEREST RATES

- US AND CANADA MORTGAGE RATES

- STOCK AND BONDS

- CHINA WILL CRASH THE WORLD MARKETS?

- POWELL NO LONGER USES THE WORD TRANSITORY…

- BITCOIN-WHO GOT WIPED OUT

USA

- US REAL ESTATE

- 30-YEAR MONEY 20-YEAR RECORD

- US INFLATION 7%

- US DOLLAR

CANADA

- MAJOR CANADA REAL ESTATE MARKETS

- CANADA DOLLAR

- UBC LAUNCHES WEALTH TAX REPORT

- THE NUMBERS, THE NUMBERS – DECEMBER 2021 and Y-T-D 2021

- VANCOUVER, WESTSIDE, SURREY – HUGE SF HOME PRICE INCREASES

- THERE ARE NO LISTINGS

What and Why is Ozbuzz watching?

We are only (and have been since 1993) interested on what impact stocks, bonds, immigration etc., etc. may have on real estate values – mostly in Canada and the US. If immigration rises, where are they going? Values grow where people go. If interest rates rise, real estate will be affected. If recreational real estate crashes, city values crash is not far behind and vice versa.

So, we do not really care abut the relative performance of other markets. But when stocks crash – as they will this year, some money will flow out of real estate. Bitcoin crash wiping out millennials. Where did they buy and did they apply a 10x? We only care of what impact other economic events may have on our real estate portfolios. So, we mention commodities because we feel that they determine primarily economic performance, deflation or possibly inflation. However, financial money creation can only have one outcome – higher inflation of hard assets eventually and always.

QUESTIONS, QUESTIONS

We received SOOO many questions last month. From questions on the ‘cooling off period’, the ‘speculation tax’ on rentals, the new wealth tax proposal, interest rates (23), ‘forecast eclectic outcomes’, ‘inflation (49)’. Also, several personal situation questions. Well, we were overwhelmed. I have not been able to answer all. I am – for this issue – highlighting the question topics. If you asked a question and have not received an answer (either from ozbuzz.ca or askanexpert.ca) don’t be mad – get even: send it again. Cheers.

Inflation/ Deflation

Inflation is now visible to everybody. Thus, I have received several “ok, I see it, but what now?” letters. Also, some ‘thank you – we stayed the course’ – letters. One long term associate, who I literally had to order into “his good fortune”, bought this special house ($580,000) in Surrey, just sent me his assessments ($1,672,000) … with no comments. I answered: “Where is my scotch?”

To the “what now” crowd, I can only say…join the crowd. We always have the blow-out inflation in real estate prices in the major cities (of the world!), higher prices then spread into cottages/holiday homes and smaller centres…and then we have an -often sharp- reversal, build a new bottom and then head up further.

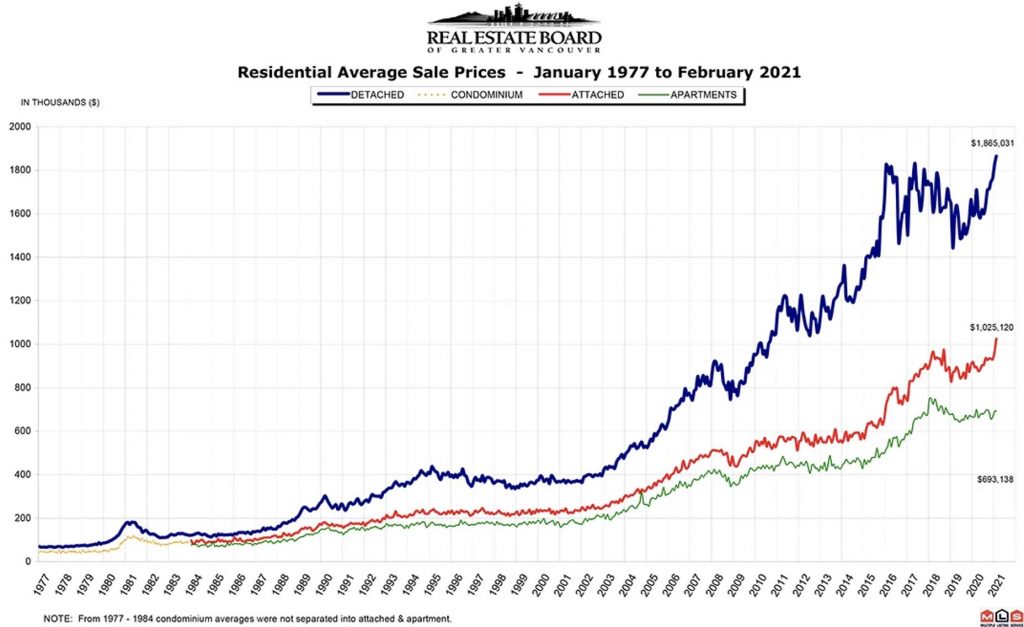

Look at the chart (detached, condos, attached) 1977 – 2021. And remember that in 1963 the average price of a single-family home was $13,500(!)

It clearly shows that my mantras (inflation, timing, trends, cycles) must matter to the short-term investors. Long term guys and gals? No matter what … prices will be higher … (in my view) in direct relation to the creation of money. Please note that the $1,865,000 price from Feb 2021 now went over $2 million!

But the dips are real. These come about because inflation hurts people visibly and governments then MUST take action. The only way they know how to do that effectively is with higher interest rates. That is where they (governments) and we are now. We now expect rates to go up sooner than later. See below. No one talks ‘transitory’. anymore…

Inflation is rising fastest in 4 years. 7% in December in the US makes it the highest rate since 1982!

Yes, our call: This time the Fed will tighten. Inflation at high. Very tight labour market. Mid term elections. They want the soft landing. Will they get it? Not likely – see below.

Remember, inflation actually helps the governments of the world… makes that enormous debt less visible. It helps to pay back real debt with money created out of the blue sky.

Major Point: Inflation? Yes, long term for sure…short term, watch government actions (see below). If the Fed and BOC do not tighten via higher rates – and they talk tighten but have not yet started – inflation will stay at about 6-9% all year, as well and likely all of 2023 and into 2024. So, they will tighten, but how and when exactly? The gurus are in conflict. Agreeing that rates must go up, they disagree as to when and how often and by how much each time.

Review our take on rates. Odds are for a sharp ‘something’. Peaking real estate prices, collapsing stocks. Much higher rates…all are on the table. Guess what? You get to choose!

Interest rates in general

Between 2008 and 2014, the Federal Reserve printed more than $3.5 trillion in new bills. To put that in perspective, it is roughly triple the amount of money that the Fed created in its first 95 years of existence. Three centuries’ worth of growth in the money supply was created out of thin air almost overnight. The money poured and poured into our financial system and pressured demand for all real (hard) assets, as paper deflated. So, soaring stocks, corporate debt, commercial real estate bonds and bitcoin. driving up prices across all markets. Inflation clocking in at 7% in the US, 19% in Turkey and even in Germany where electricity prices are now 43% higher than the EU average.

So, we know that we have been printing money like crazy since 2008. We can also see the result. In my 1998 book “Forget about Location, Location, Location” I published the page of that book and my Canada Real Estate book (2009) in my Ozbuzz 58. (Deflationist? Read it and weep.)

I predicted more inflation. I predict it still now – long term. But with rising rates, QT – short-term trouble ahead. The peak in RE prices is in.

The US Fed agrees. No more nonsense ‘transitory’ remarks, now the Fed hinted a few times that they may be rising rates. Well, now the Fed is being believed. The much higher (7% reported) inflation has governments worried. In our opinion it is actually MUCH HIGHER (go to shadowstats.com). Goldman Sachs foresees four massive interest rate hikes from the Fed this year. It’s mid term election year and in our view the US will launch the announced 3 x rate increases as early as March (RBC astounded the Canadian world by predicting the BOC doing 5 raises starting Jan 26!) Of course, the famed Benjamin Tal predicted a few weeks ago 6 raises.

Ok, the democrats may well be on the way out, if inflation stays where it is. So, rate increases (to bring down rate of inflation) are far more likely now…and that is what Bitcoin (down 41%!) and the Nasdaq are signalling.

I wrote last year and the year before to watch when 10-year rates go over 2%, the world’s rates and with it the economy will change. The 10-year rate touched 1.8% on Friday the 7th. The 2-year rate is highest since March 2020. So, keep watch. When fed tightens future financial conditions and inflations goes down.

The biggest fear? The FED and BOC will blink – as we expect the high rates of inflation to continue and raise rates too fast (the proverbial massive black swan!).

Fact is: The yield on 2-year treasuries has gone from 0.11% in early 2021 to 0.8% today; and from 0.22% from just last September. That’s a massive collapse in prices. And this is with the FED still buying a good chunk of them. How high will the yield be by March, when the Fed buying stops? It’s obvious that nobody wants to buy treasuries at anything close to today’s manipulated rates. Inflation at almost 7% changes the goal posts.

Major Point: Look at current mortgage rates below. Use them, get safe, we are speculating/guessing like all of the world’s financial commentators all around us. No one knows (maybe not even the Fed), what exactly it will do! When Powell went into Quantitative Tightening in 2018, he did an about turn in a month with abject fear – as stocks tumbled. (Re-read Jurock Real Estate Insider December/January 2018/2019).

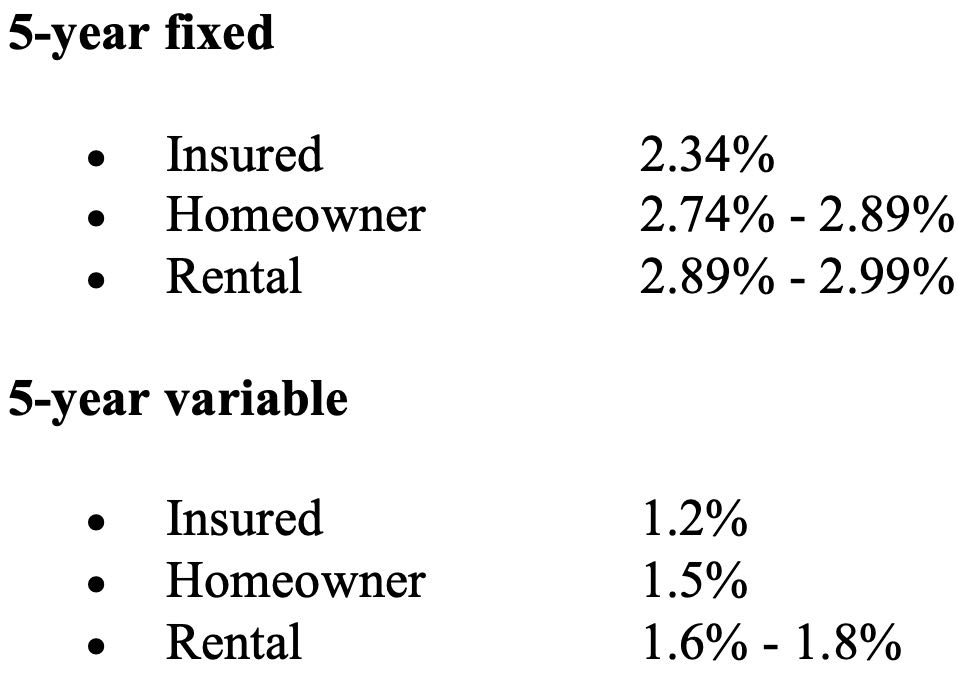

MORTGAGE RATES

In the US rates have been clocking in at the highest in 2 years. US 30-year rates are going up to 3.23 percent – highest since May 2020. May well impact US housing markets. To the extent that rates have a psychological impact, higher rates will slow down housing. Kyle Green advises current rates as follows (supplied by Mortgage Ace Kyle Green):

Advice:

- Definitely get pre-approved – bonds may have another hike in the next few months.

- Rental property down payment still only 20% down … rates rising, qualifying more difficult.

- Values have gone up, may be a good time to refinance and get a HELOC to re-invest into something else. (This is from Kyle, who is likely right. Ozzie not keen on HELOC – Black Swan.)

Write Kyle, review your portfolio and (maybe) lock in your rates: info@greenmortgageteam.ca

Bitcoin

Bitcoin and 10-year treasuries travelled together – until the FED took a more hawkish stance. Now they have diverged … given Bitcoin its worst start to a year. Perhaps Bitcoin holders now look at the rise in interest rate as a given … Bitcoin dropped below $40,000 on Jan 10. Why the turmoil in Kazakhstan? And, who cares? Many reasons, but … they can print (create) 20% of ALL crypto mining. In that mickey mouse country? A fifth of all crypto is produced here. That’s scary to me.

We got a lot of response to our piece on 5 xers or 10 xers. Bitcoin dropped 40% in a month. Ask yourself? How many millennials were holding the debt? I’d say most of them got wiped out with huge debts to boot. The big boys, the funds, they did not get the losses. They helped drive the price down and then re-bought in the low forties. From $69,000 to $40,000 in a month. Arrgh!

Think about Bitcoin where it is created:

20 percent Kazakhstan, 10 percent Russia, Canada 10 percent, US 35 percent…the rest small countries. I only would rely on Canada and the US … the rest? You my dear crypto gal … get to decide what it means to your wallet.

For balance: Google the man from Omaha – Warren Buffet – and his interview from December. He called Bitcoin – turd.

STOCKS

WHEN BIG BOYS RUN – GO HIDE! Watch what they do, not what they say. I could write a book as to what Elon Musk and Bill Gates said they would do and what they predicted would happen – only to see them do the opposite. Famously in 2020 (while arguing the opposite in public) Bill Ackman pulled off a ‘big short’. This trade took only about 1 month to pay-off $2.6 B.

Big billionaires (Musk, Zuckerberg, Bezos) sold some $69 billion last 2 weeks (last 2 weeks!). Elon Musk calls for 2022 crash yesterday … Ah so, sell and then predict!

Well, you and I know, billionaires like to sell high and buy low. Now they are selling. Even Michael Burry reportedly sold 94% of all of his holdings.

Parallels to 20’ or 90s? Excess liquidity, rising prices and big guys running away. Selling out before the Dot.com. That crash wiped out $1.7 trillion worth of capital out of the market.

Clearly, when rates rise there will be a blood bath on Wall Street.

The crash in the NASDAQ tells the story as well. Its actually an incredible crash. Hedge funds sold their tech shares at fastest pace in 10 years between Dec 30 and Jan 3. In fact, the biggest sell off since data was collected.

And then:

More than 40 percent (40%) of the Nasdaq shares are down 50% or more! Funds like ARK are also down by 45%. With record amounts of debt everywhere, the market participants (big boys – not the 5xfor or 10 x crowd).

Finally, big local billionaire (he who beat Twitter’s lawsuit).

Frank Giustra: “The Fed will halt asset purchases by March and hike rates in June- . but they will never take rates much past 2%, because they cannot. I predict with that inflation here to stay, we will be in a negative rate environment for a long, long time.”

We think not but, if he is right, inflation will soar. OK, make up your own mind… but spend an hour on YouTube…and get really confused.

Major Point: If you need to be in stocks… note the Nasdaq above. Buy dividends, buy income. Get out of most tech which promise capital gains but show no way of making money operationally. Finally, bond holders will get hurt in rising rates. Review your portfolio with your broker.

VOLATILITY EXPLAINED

There will be more of it. Day traders delight. For the BEST day trader views subscribe to Victor Adair’s fantastic blog at http://www.VictorAdair.ca. So far it’s still free. I never talk US dollar, interest rates etc. without checking his latest -every Friday- blog first.

US DOLLAR

You know our view of the US dollar being the reserve currency of the world (yes, it still is) and staying stronger. Crazy currency collapses in Turkey, Venezuela, etc. , etc. will make it even more so. For those that argue trade deficits: It’s true that the US reported an $80 billion trade deficit. However, in my view that means an even stronger dollar. Generally, when trade deficits are widening, the Dollar goes higher. (When we export more than we import it means more dollars are needed to pay and we are exporting the dollar too.) When the US raises rates, they will attract more foreign buyers/investors, which will still strengthen the US dollar. (The sharp rising Volker rates in the 1980ties designed to slow down inflation saw a huge increase of foreigners rushing into the high interest paying US dollars driving it even higher. Think: Germans get negative rates; the US now offers 1.8% (more increases coming?) The US dollar will be higher with fluctuations in energy!

CANADIAN DOLLAR

We see the Canadian dollar still tied mainly to oil and commodities. As oil will fall (after the winter) we see the Canadian dollar come down. A lot of other commodities (like lumber down 50%) are heading lower when rates go up. A recession looms.

Snapshot:

- Recession 70 percent likely

- Inflation higher long term

- Real Estate markets will be peaking after the 4th rate increase

- Bitcoin – you decide

- Interest rates- higher

CANADA REAL ESTATE

Watch where you buy in Fraser Valley and all ‘fire, smoke and flood’ areas in Canada. Insurers will not be keen to lend. All common area insurance will be dramatically be higher. When buying a condo, check when insurance expires. At that date expect 100% increases to all insurance portions of strata fees. Watch for inflation news.

Check the availability to get insurance before you sign. Some CUs don’t insure Chilliwack e.g.

US REAL ESTATE

Higher interest rates, higher dollar, all will have an impact. Safe are low tax states (Arizona, Texas, Florida – although Canadians can’t get storm insurance and taxes are higher here). Worse off will be California, NY, Jersey, Chicago etc.

Note: Wells Fargo cancelled credit lines (check Ozbuzz 48) and we now hear of a lot of US insurers changing their rules. Some carriers will not underwrite homes over $3 million (E & O). Also, homes valued over $2 million need to be separately underwritten (spread the risk). Rising rates and inflation expectation, will change rates for unusual (high price) and multimillion dollar properties.

Mortgage rates are rising, but several reports show US median values are still relatively low (as opposed to Canadian). For instance, the average US house – buying is cheaper than rent – according to ATTOM’s 2022 Rental Affordability Report. They say that owning a median-priced home is more affordable than the average rent on a three-bedroom property in 666, or 58 percent, of the 1,154 U.S. counties analyzed for the report. That means major home ownership expenses consume a smaller portion of average local wages than renting. Home ownership remains more affordable even though median home prices have increased more than average rents and more than average wages.

“The neighbors always leave their sprinklers on, which is a little bit annoying. It’s a source of constant irrigation.” -LaffGaff.com

NEW YEAR GOALS

For some 20 years I led a Real Estate Action Group. I sold it several years ago, but what we did at every first meeting of the year was a “goal setting” session … of what we needed to commit to do for the new year. Our Motto? COMMIT – PERFORM – MEASURE!

Not a NY resolution. NO, rather a serious of specified actions we need to take and be committed to in several areas of our real estate investing world.

That’s what I like to leave you with for 2022:

Don’t do resolutions and business plans that you are not committed to. The world’s office drawers are full of finally laid out and neatly typed pretty business plans.

Nope! Only write action plans with specific actions to be accomplished with a starting and finish date. A goal without a deadline is just a wish.

Stop wishing – commit yourself – do it – and review your actions weekly.

CANADA REAL ESTATE

Two years ago, I quoted a report that CMHC had commissioned UBC to do a study on the capital gains tax exemption. They denied it but last year had to admit it and here it is: A proposal to tax everybody that owns a home over $1 million. Since the average price of a home is $2 million in Vancouver this could be a substantial bite out of your ‘tax free’ capital gain … or actually you don’t have to even have a gain – you would be taxed.

Writes writing Ace Frank O’Brien in the fine magazine “Home Builder”:

“A report from a group partly funded by Canada Mortgage Housing Corp. (CMHC) is calling for tax on homes priced at $1 million or more.

Advocacy group Generation Squeeze released the report entitled Housing Wealth and Generational Inequity, which explored policy incentives to solve Canada’s “housing unaffordability crisis.”

Among the recommendations was the call for a tax that would range from 0.2 per cent for homes valued between $1 million to $1.5 million, and up to 1 per cent on homes valued over $2 million.

The annual tax would be deferrable, meaning the accumulated total would not have to be paid until the home is sold or inherited. According to the report, a home valued at between $1-1.5 million would incur an average annual surtax of $408, while a home valued at over $2 million would average an annual tax payment of $14,710.”

You figure it out, .02% of a million. How do we get to $408? Also, we think 1% on 2 million comes to $20,000. How do we get to $14,710? Anyways, lets stay simple. The average price of a house in Vancouver clocks in at 2 million. That’s a fact! So, after 10 years this tax would come to $200,000! Virtually every homeowner in Metro Vancouver and Greater Toronto, where the composite home price is in excess of $1 million is affected.

The crazy thing? What if you don’t make a profit in any one year? Just pay the tax!

CMHC stated in an email to HOME BUILDER.

“Our government has clearly stated several times that we will not be introducing a tax on the equity of primary residences in Canada. Any suggestion otherwise is false,” said CMHC media manager Leonard Catling in releasing a statement from the Ministry of Housing.

However, a BC government source pointed out that this proposal is similar to the NDP school tax increase on houses over 3 million. But it needed to be studied!

Major Point: As I wrote in last month’s Ozbuzz. The new law of buying a home and selling it within the first year makes the whole gain taxable. This is the ‘thin edge of the wedge’. It will be considered income. So, not even capital gain, but income. In a way, that is a real step to the ultimate goal … tax the gain. (Next year make it 2 years, then 3, etc.?)

GENERAL CHANGES AHEAD:

Remote work is here to stay. Larger homes preferred.

Inflation is here to stay – but a recession is ahead. So, price higher? Yes, but later

The high of the market is in place.

Migration, where do people move to?

People move yes, but mostly to smaller cities.

Some move back into the cities by people missing the action.

Check out lifestyle cities (Coastal or lakes or mountain).

Stay away from fire, smoke, flood areas.

Get pre-approved – lock in interest rates.

Condo markets stronger in 2022 – read minutes, expect much higher condo fees.

Why are there no listings?

The biggest reason is that owners are sitting on crazy profits. In Surrey $350,000 a year – 2 years in a row, and with that kind of performance, why move?

- There is also nothing much available when they go out to look.

- Some also worry that they leave further profit increases on the table.

- People are holding on to the real estate they buy.

- It will continue for a while.

- Inward migration accelerating.

- Increased students coming back.

Since there are few properties for sale … people are back to multiple offers. This picture will change with a possible “crash’ in stocks, much higher interest rates and faster increases and more often than expected.

Major Point: If you are staying, fix your rate. If you want to move, get some quotes now and watch the interest rate market! Need a realtor, I can recommend some.

THE NUMBERS

TORONTO

Similar to Vancouver, there are few listings in the whole country. Toronto, for instance, a city of 6.5 million, has just 3,200 homes for sale, that’s less than half the 7,900 on the market a year ago citing the Toronto Regional Estate Board.

Blame low interest rates. Home sales in TO surged by almost a third last year to more than 121,000, sparking fears of a bubble and breaking a record set in 2016. Average home prices in Toronto jumped 18 percent last year to about $1,095,475, also an all-time high.

BC

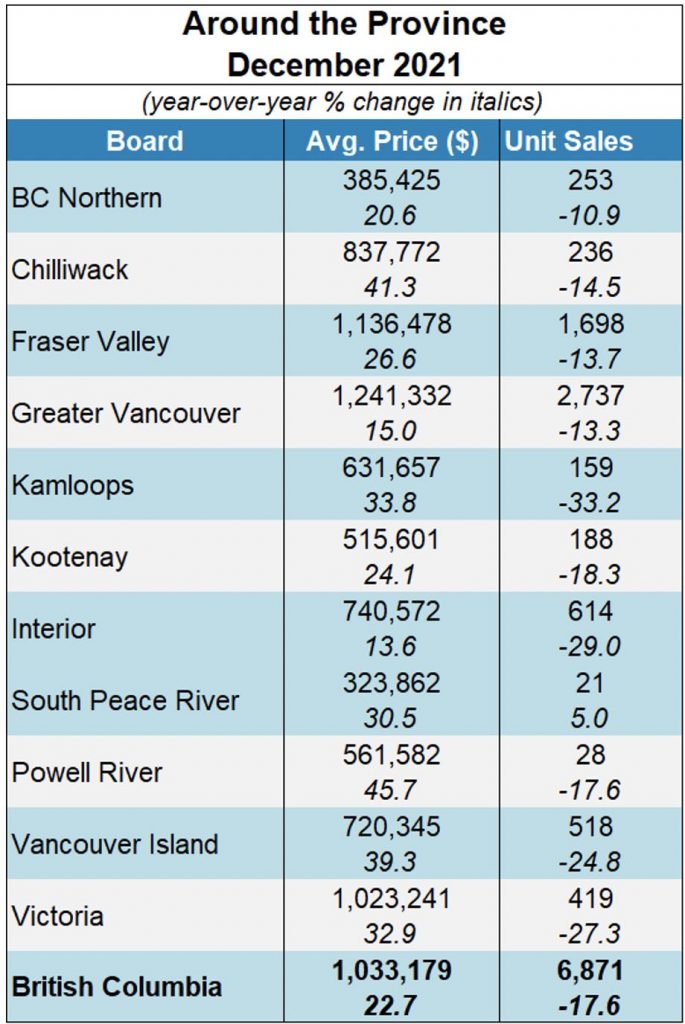

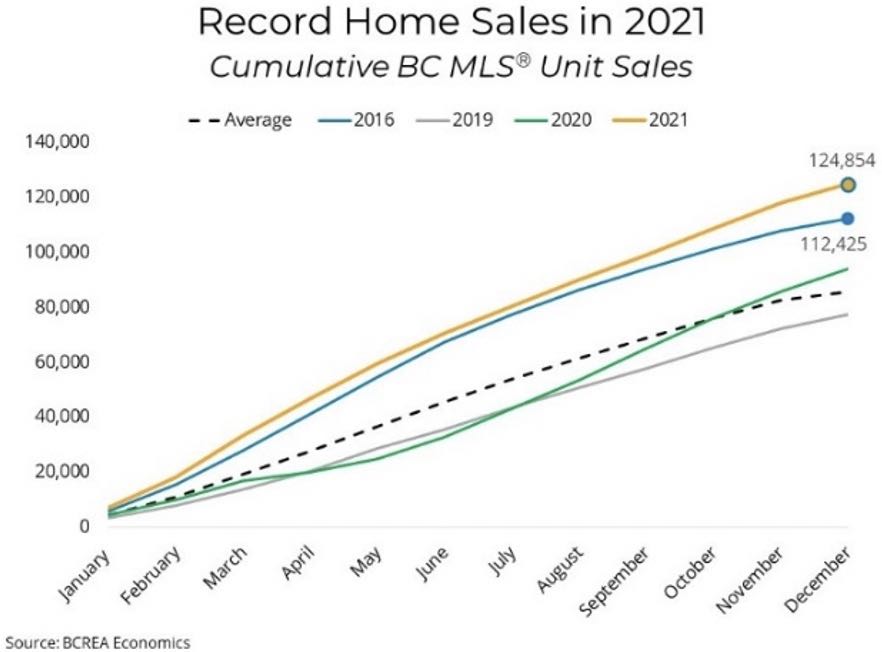

The British Columbia Real Estate Association reports a record 124,854 residential unit sales a 33 per cent increase. The annual average residential price in BC was $927,877, a 19% increase from $781,572 recorded the previous year.

“Last year was a record year for BC homes sales with seven market areas setting new highs,” said BCREA Chief Economist Brendon Ogmundson. “Listing’s activity could not keep up with demand throughout the year. As a result, we start 2022 with the lowest level of active listings on record.”

6,871 sales were recorded in December down 18 per cent from a record-setting December 2020. The average MLS®residential price in BC passed the $1 million mark for the first time as the average price in three of the largest markets in the province were over $1 million in December. Total active residential listings were down 41 per cent to a record low of 12,179 units. The supply situation is particularly concerning in the Fraser Valley, Chilliwack, and Vancouver Island where there is one month or less of supply at the current pace of sales.

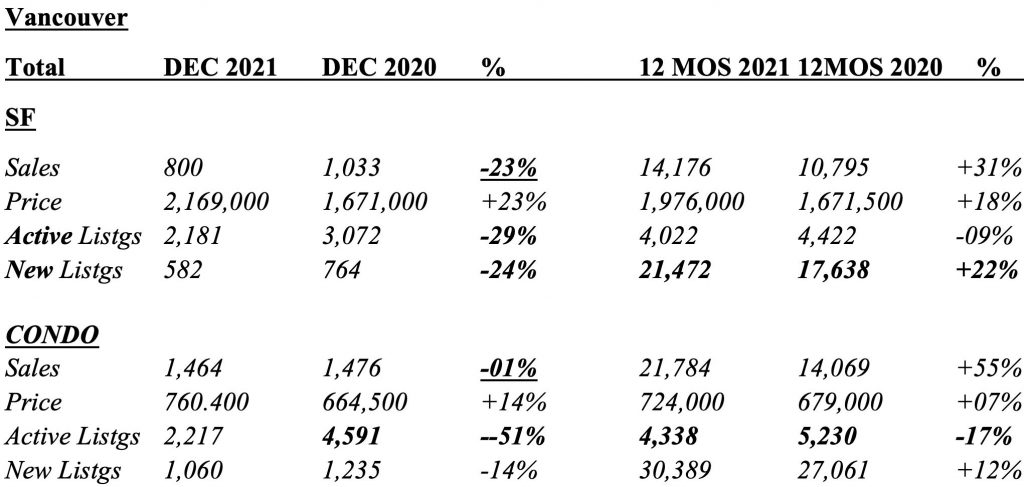

VANCOUVER

NEW STATS. The month of December 2021 as well as the entire year of 2021 measured against the entire year of 2020.A detailed look at Vancouver, Westside, and Fraser Valley.

Several long-term subscribers reminded me of our ’20-year plus’s year-end summaries going right across the country and for several years. Well, I reminded them that those were paid subscriptions and that this one is only paid by your friendly sign-up. I will however take a look today against the running total of the year 2021 plus the usual monthly totals.

Some interesting things emerge:

Sales continued to surge in 2021 to an all-time high of 43,999 (up 42% from the 30,944 sales last year) And imagine this: 74% higher than 2019 (sales clocked in at 25,351).

Vancouver had a crazy fall. December was no exception, but things tightened up.

Sales of SF homes were down by -07% in November but down by 23% in December. But December home sales in Metro Vancouver were still 33 per cent above the 10-year average for sales.

SF home prices are still up by a whopping 23% (!) Up by $600,000 since 2019! But against the running 12 months total the increase came in at only 18%.

SF listing and condominium active listings are both down by 29% and 51% (wow!) respectively!

However, last month’s new listings were down 30% month over month but rising on a year-to-date basis. We actually had some 22% more new listings in the SF sector and 12% in the new condominium listings area.

Study the numbers, they foretell the spring market!

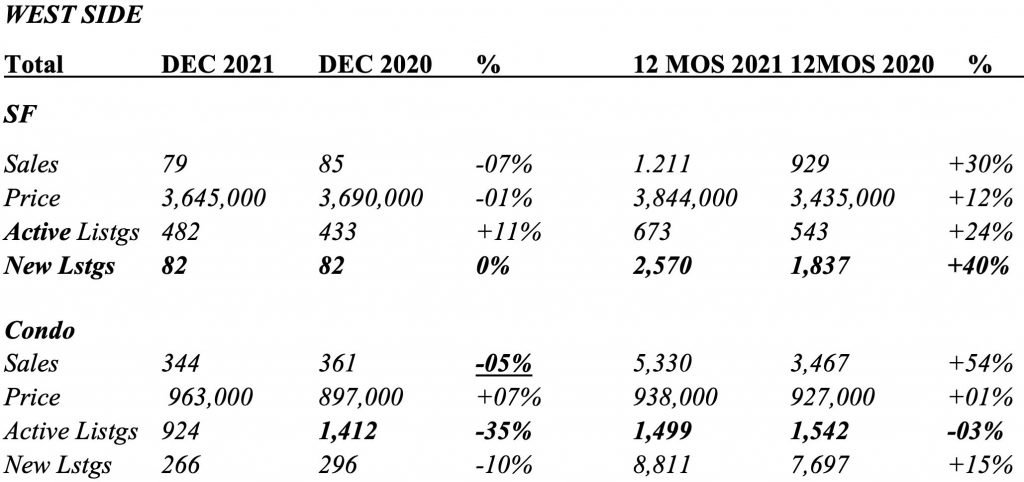

Vancouver Major Point: The Westside SF price dropped from $4,325.000 in November to $3,645.000 in December. Likely only a few sales making up these numbers. This ‘mini crash’ saw the average price drop (only 1%) for the first time this year and – more importantly – drop the average SF price annual increase to only 12% (versus 37% for Surrey). Notably the westside condominium prices (already exceedingly high) only rose by 7% in December and for the year? Only 1%!

MAJOR POINT:

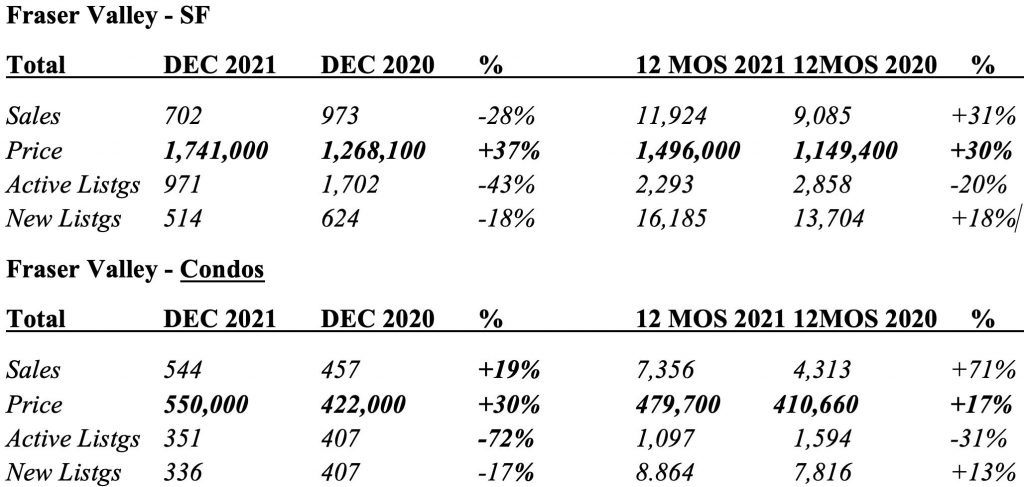

FV December SF sales continue down sharply by 28% over 2020.

But SF Prices are still up an unbelievable 37%. At the same time Surrey SF Active listings are down by a whopping 43% again.

Condominium sales are up by 19%, the average condominium price is up a strong 30% (WOW) and active listings are down 72% (really?)

The ‘Jurock Case Investment Realty (JCIR)’ recommendation to buy Surrey and Whalley and the whole market for years … has paid off for the ‘ACTION INVESTOR’ . If you would like more info on upcoming events sign in at www.jcir.ca

Come to the World Financial Outlook Conference with Martin Armstrong and a dozen speakers:

Ozzie, Michael Campbell, Michael Levy and Victor Adair and guests are now on podcasts every week: https://omny.fm/shows/money-talks-with-michael-campbell

If you are in building, selling, marketing, developing, lawyering, etc. list yourself in the free BC real estate directory: www.bcred.ca (11704 visitors in September)

- Questions to Ozzie and experts: www.askanexpert.ca

- Set up your own “talk” at www.realestatetalks.com (30019 visitors in September) (Ozzie’s 23-year-old bulletin board for you to play in)

Want to see all Ozzie blogs and all Ozzie podcasts? Go here: www.ozbuzz.ca

Who the heck is Ozzie? Go to www.ozziejurock.com

Ozzie on YouTube? www.youtube.com/jurockvideo

Ozzie’s zoom economic/motivational speech to your company or organization?

Go to www.ozbuzz.ca to inquire rates and availability.

Your thoughts – AS ALWAYS – are most welcome. WRITE QUESTIONS HERE: INFO@OZBUZZ.CA and put Oz Buzz in the subject line. I try to answer ALL questions, but not all will be featured here.

People do not do what

You expect, they do what

You inspect – with respect.

I set the values

I set the standards

I hold myself and

Those that report to me accountable

I expect adherence…

I inspect with respect

I find someone to inspect me

I will grow into my future best

DISCLAIMER

Please note that any response to any email or any invitation to any meeting is accepted on the understanding that “Jurock Real Estate Insider (JREI)”, “Oz Buzz (OB)”, “JCIR (JC)” as the case may be, are not responsible for any result or results of any action or actions taken in reliance upon any information contained in this posting or meeting, nor for any errors contained therein or presented thereat or omissions in relation thereto.

It is further understood that the said OB or JREI, or JCIR as the case may be, do not, pursuant to this posting, purport to render legal, accounting, tax, financial, planning, or other professional advice. The said OB and JREI and JCIR may or may not own properties discussed at meetings or receive or not receive referral fees at any meeting you may attend as a result of this posting or invitation. The said OB and JREI and JCIR, as the case may be, hereby disclaim all and any, liability to any person, whether a purchaser of any offering, a reader of any offering, or, otherwise, arising in respect of this postings and of the consequences of anything done or purported to be done by any such person in reliance, whether whole or partial, upon the whole or any part of the contents of these postings. If you respond to any posting OB or JREI and JCIR or attend any meeting from and by said companies, we fully expect that you get independent legal/tax/investment/mortgage advice as the case may be.

WANT TO PARTICIPATE?

Go to www.realestatetalks.com – Some 2,500 members (47,009 posts) talk real estate. Ozzie created this bulletin board in 1998!

If you are in a real estate related industry of any sort (realtor, appraiser, lawyer, home inspector, etc.) list yourself in Ozzie’s free British Columbia real estate directory at www.bcred.ca.

OZZIE’S YOUTUBE CHANNEL

You can watch all videos and podcasts on my YouTube channel at https://www.youtube.com/jurockvideo. It is a great way to check on what I said 10 years ago.

Moneytalks Podcast

Ozzie, Michael Campbell, Michael Levy and Victor Adair and guests are now on podcasts every week: https://omny.fm/shows/money-talks-with-michael-campbell

OZBUZZ.CA

Why subscribe if I can just go to the website at Ozbuzz.ca? Hot properties and the latest podcasts are DISTRIBUTED TO SUBSCRIBERS FIRST– posted 2 weeks later on website.

HAVE A QUESTION OR COMMENT?

You can reach me at info@ozbuzz.ca with all of your questions, comments and concerns regarding the Oz Buzz publication.

Oz Buzz Podcast

Disclaimer

Subscribe

| Subscribe to Oz Buzz: |

(You’ll get Oz Buzz 2 weeks before it’s posted online)

As being new in the sellers market people tend to make a lot of mistakes which is understandable. I hope that these tips will make it easy for the people who are making such mistakes. If that happens that it would be great.