“There is no art which government sooner learns of another than that of draining money from the pockets of the people.” –Adam Smith

June 6, 2022

TOPICS

- DOWNRIGHT SCARY HEADLINES

- ELITE SAYS HURRICANE IS COMING THIS SUMMER

- INTEREST RATES EVEN HIGHER

- ASTOUNDING 63 PERCENT CRASH IN SF HOME SALES.

SALES CONTINUE TO PLUMMET IN VANCOUVER AND THE VALLEY - THE NUMBERS: MAY 2022, 2021, 2020, 2019

- BUYERS LISTEN TO THIS

- REALTORS LISTEN TO THIS

- FIRST-TIME HOME BUYER INCENTIVE

- BITCOINS, ALTCOINS, SCAMS GALORE

- STOCKS CRASHING

- CHINA CHIEF XI SAYS: SELL ALL OF YOUR HOUSES IN VANCOUVER AND ELSEWHERE

- MILLENNIALS ARE LOSERS IN CRYPTO – NOW LOSERS IN REAL ESTATE?

- STRESS TEST SECRET

- INTEREST RATES .75% COMING JULY 13?

- WHAT TO WATCH ON JUNE 10

- QUESTIONS, QUESTIONS

- SONG/MUSIC OF THE MONTH – OK, NOT EVERYONE’S CUP

OZZIE THOUGHTS

Some of you have been waving a friendly but firm finger: “Don’t get negative. Ozzie.” Well, I am not ‘getting negative,’ I share opinion, formed through vast experience (yep), through various cycles and my opinions are based on my (shared with you) principles.

So, wither the markets? Short term: Continued down. Long term all hard assets higher once we have gone through the valley!

To me the numbers speak for themselves. Anecdotally, some Realtors tell me of “no showings in 3 weeks, lowball offers, developers’ enormous incentives”, etc.

The HEADLINES and the numbers tell a somewhat scary story.

WHITHER THE MARKETS IN THE US AND CANADA?

ECONOMIES – INTERNATIONAL – ALL POSSIBLY IMPACTING OUR MARKETS

SCARY HEADLINES

ECONOMY

- ELON MUSK has a “a super bad feeling about the economy”

wants a 10% job cuts at Tesla. - JAMES DIMON – “There is s hurricane coming. We are preparing for it!”

- BANK OF AMERICA says: “The summer from hell is coming”

- BLOOMBERG: “Worldwide global wealth is down 14% gone!”

Major Point: Even if we disregard the “YouTube naysayers,” it is hard to disregard these!

BITCOIN AND STOCKS

Most crypto is junk! (Out of 18,000 coins).

Full of scams. US Federal Trade Commission:

Since the start of 2021, more than 46,000 people have reported losing over $1 billion in crypto to scams. The top cryptocurrencies people said they used to pay scammers were Bitcoin (70%), Tether (10%), and Ether (9%).

Crypto winter.

The crypto market has lost roughly $1 trillion in value year-to-date in one of the worst selloffs in the maturing market’s history this year.

Just Bitcoin had a $2 trillion market cap, now down 60%.

Losses are staggering.

Robinhood high $85.00 – on June 2 $9.17

Coinbox high $ 369 $67

AMC high $73 $12.50

MAJOR POINT: Staggering losses make a big sucking sound to the real estate buyer market. If most of the crypto money was lost by millennials – they have no money left to recover – in fact have huge loans to cover losses at 2x, 5x, 10x (see previous Oz Buzz).

STOCKS

Of course, it is not crypto losses alone.

Last week marked the Dow’s first eight-week losing streak since 1923, while the S&P 500 capped a seven-week losing streak, its worst since 2001. The Nasdaq saw its seventh negative week in a row for the first time since March 2001. The tech-heavy index also saw its lowest intraday level since November 2020 on Friday.

- CNBC: $35 trillion lost in market value in 2022

Just US stocks lost some $7 trillion in 2022.

As we said last month more than 50% of the Nasdaq lost more than 50% of their value!

Individual stocks? Netflix hit a high of $700 and now it is $199 (down over 70%).

To outsiders like me it looks like stocks go down on good news and up on bad and then turn on a dime.

Overheard at the party: “If you put in a trillion into the consumers hands and then all of a suddenly take it all away, we will cause a disruption.”

Major Point: I do not make any stock market predictions other than: It will get a lot worse, there will be no V-shape return. Question is: Who lost it? I say likely your real estate buyer.

FOR THE BEST WEEKLY STOCK MARKET ADVICE FROM AN ACE DAY TRADER! GET VICTOR ADAIR’S PERSPECTIVE, GO HERE: VICTORADAIR.CA (STILL NO CHARGE)

INTERNATIONAL

Similar issues worldwide:

GERMANY

VW is down 30% in sales in April

- German PPI 33%

- 8.7% inflation in Germany

- (Politicians tell workers “Don’t strike’

- Gas up 49% and food up 30%

CHINA

- Economic trouble – covid related and real estate crash continued

- SHANGHAI sold not even one EV last month.

China chief XI tells people to sell their houses in Vancouver (AND EVERYWHERE ELSE!).

- Actually, his ORDER is to his cadre and their RELATIVES to sell all business investments and real estate outside China.

- Twitters Mortimer: If you believe sellers are being truthful… (and we know many are not)… about 18% of current Greater Vancouver real estate listings are listed as being “vacant”. Early Chinese sellers or idle speculation?

EXTRAORDINARY MAJOR POINT:

Here we have Trudeau forbidding foreigners to buy Canadian real estate for two years. Now China orders its citizen to sell their Canadian real estate. Why? Unintended consequences. China/others saw what happens when the WEST puts out sanctions to other countries’ oligarchs and governments. This will change the way the US dollar is looked at (as a reserve) and why China does not want its top guns exposed. If you plan a war (i.e., Taiwan), or, etc.

THE UPSHOT – FINAL, FINAL MAJOR POINT:

- We are in uncharted waters worldwide. Economies teetering, inflation rocketing, indebtedness soaring, interest rates soaring.

The elite is scared, the non-elite (us) has lost their collective shirts in stocks and crypto. Prices are falling. Look at the numbers and study the last 4 years and particularly the last 4 months. OK. I have NEVER been outright negative before… We hate to be negative but get safe! See predictions below. I remain bullish on real estate in the long term (inflation is here to stay, you know). But short term be very careful … see recommendations below. - Stocks are in free fall; real estate is reversing and all that on the “minimal” interest rate increases. Yet, the big change is still to be felt. Quantitative Tightening started on June 1. Will not show instantly BUT huge liquidity problems lie ahead. QT will have a major impact. QT means – even more – VOLATILITY!

- Get into more cash.

CANADA

INTEREST RATES

Another .5% increase to the overnight lending rate to 1.5% – just below pre-pandemic level of 1.75%

We expect another a minimum .5% on July 13. The bank will watch how we react to buying and selling things in general and real estate in particular. The consensus is that after that increase the bank will slow down. My view is that they will increase further. If inflation stays near 7%, the BOC may go to .75% next time.

Even if only the US on June 10 clocks in over 8.3%, hang on to your ‘interest rate hat’.

I wrote in February that we hoped the bank would go slowly (start early with a .25% increase and stay with that). We worried that the bank would go too fast. Now they are playing catch up. BTW instead of 6 x .25% over a one-year period, we will have had the same 1.5% in 4 months.

BOC has not raised its rates more than .25% at a time for over 20 years prior to 2022

Its not the raising rates, it is the speed of the raise…both in the US ( 30-year mortgage from 2.7 % to 5.6% in 4 months and in Canada – that is worrisome

UPSHOT?

- Variable rate mortgage and/or a Home Equity Line of Credit, interest rates will rise accordingly (.50%). About $28 per $100,000.

- Qualifying for home equity lines of credit and some variable-rate mortgages will be harder.

- A borrower can expect to lose just over 8% of their borrowing power on a HELOC compared to the beginning of 2022.

- The stress test of 6.2% makes it worse.

HIGHER RATES: THINGS TO WORRY ABOUT:

- Presales and commercial transactions are a growing concern.

- Commercial properties are worrisome if there is a business downturn. If the net operating income does not increase at least to cover rising rates, lenders will get nasty – as in the past.

FIRST-TIME HOME BUYER INCENTIVE

A program we have not heard about much – since its launch in 2019 is now being ‘changed to help buyers more’? OR? Is Ottawa trying to limit possible losses if home values take a big dive?

1. The First-Time Home Buyer Incentive is a shared-equity mortgage with the Government of Canada, which offers:

- 5% or 10% for a first-time buyer’s purchase of a newly constructed home

- 5% for a first-time buyer’s purchase of a resale (existing) home

- 5% for a first-time buyer’s purchase of a new or resale mobile/manufactured home

The shared equity component of the incentive means that the government shares in both the upside and downside of the property value. In other words, if the home has increased in value, you will need to pay back more than you borrowed. If the home has decreased in value, you’ll pay back less than you borrowed. Not too many people took up the government offer – not liking the shared equity idea.

Imagine you took a $100,000 on your million-dollar house in Surrey in 2019 (10%) and now sold it at $2 million… you would have to be paying back $200,000! Nice piece of change for the government “helping” you.

So, now the government – doing a lot of thinking about the market to come (???) has extended the program but will not share as much of the profit AND A LOT LESS OFF POTENTIAL Losses!

NEW IDEA

1. First-time homebuyers purchasing a home in the Toronto, Vancouver, or Victoria Census Metropolitan Areas are now eligible for an increased Qualifying Annual Income of $150,000 instead of $120,000, and an increased total borrowing amount of 4.5 instead of 4.0 times their qualifying income.

2. BUT ALSO:

A) The Government of Canada will limit its share in the appreciation of a home! Now, homeowners will pay back up to a maximum gain of 8% per annum (not compounded) on the Incentive amount from the date of advance to the time of repayment.

B) The Government of Canada will also limit its share in the depreciation of a home at the time of repayment. This is up to a maximum loss of 8% per annum (not compounded) on the Incentive amount from the date of advance to the time of repayment.

Major Point: I know, I know, the cynic in you wonders? Why now? They are in the money? What are they expecting? Indeed … good questions.

MORE MORTGAGES

Dustan Woodhouse, President at Mortgage Architects tells me: “There are now more offers with conditions, although very strange to see many still firm and often in cases where they clearly did not need to be firm.” He calls that “Odd behaviour.”

- Fact is offers now contain more ‘subject to home inspection,’ ‘subject to financing, subject to sell my house etc. (as it should be in a slowing market)

- Many realtors still just WRITE no subjects – because buyers are not realizing the market has changed

- That is indeed odd behaviour, or lazy behaviour. Avoiding the trouble of ‘buyer changing his mind”

STRESS TEST SECRET

Innovative strategy by innovative brokers. Currently variable rate rates still need only 5.25% to qualify not 6.25% So, qualify on the variable rate at the stress test of 5.25% – lock in after.

OK, ALL BUYERS NOTE:

- Appraisers’ base appraisals on recent sales of similar properties. Thus, they are close to any market condition.

- Appraisers in a rising market generally appraise properties at what they see on the contract.

- Appraisers in a falling market see what is happening but they don’t want to follow the market values down, so they are often leading them down by making the appraisal lower than the original offer was. Understand that and get the mortgage app in asap.

Buyers quick note:

- Sales are down nationally 25% – SF sales down much higher in Vancouver – down 44%

- Sales were down in FVREB SF 63%

- Markets are slowing everywhere in North America!

- Buyers being in crypto and NFT have lost their shirts… no more buyers

- Higher rates are driving buyers out too

- Inflation, Interest Rates begin to Slow Miami Residential Sales in April, Seattle too

- Psychology on the way up is crazy. In the downturn it can also change dramatically

So

- Write offers only with subject clauses

- Inspect. Inspect.

- Apply for mortgage immediately – appraisers will be hesitant.

- Study local area stats.

OK, ALL REALTORS AND SELLERS NOTE

As a former Branch Manager, General Manager and National President of real estate companies I have had the pleasure of crazy rising and fear crazy falling markets. The markets DO repeat.

I am not giving you advice, but it pays to talk to the older guys and gals in your office and how often they have seen their sellers literally FOLLOW the market down.

Do the research for your submarket like below and have a heart-to-heart talk with your clients. When markets turned down together like this in the past (not saying they will in future), but when they did turn some owners always lowered their price just a little too late.

COMMENT: INFLATION AND TIMING

Most of them on the inflation plus timing piece. I think I did my general understanding of markets some justice with the basics. MACRO: Inflation, Timing, Trends, Cycles. LOCAL: Inward migration, interest rates, demand, and supply. Nothing to add.

COMMENT: AN EXCELLENT PIECE ON THE CRASH OF TERRA/LUNA/UST WILL CRASH REAL ESTATE. MAN THANKS!

COMMENT: REALLY LIKED THIS COMMENT FROM A SERIOUS INDUSTRY LEADER:

“OZ, I JUST READ YOUR BUZZ 70 AND FULLY AGREE. I JUST FINISHED A 3 DAYS SEMINAR WITH XXX PEOPLE OF MY COMPANIES. PEOPLE FORGET THAT THERE HAVE BEEN 33 RECESSIONS SINCE THE GREAT DEPRESSION. HERE ARE MY SLIDE AND I TALKED OF INFLATION SINCE 1778 WHEN INFLATION WAS AT 30 PERCENT IN US AND I TOOK THEM THROUGH A JOURNEY TILL NOW.

WE HAVE NEVER SEEN ANYTHING LIKE THIS.

I WILL HAVE ALL TYPES OF OPPORTUNITIES TO BUY COMPANIES AS PEOPLE GET FEARFUL. I AM GOING TO BE “MORE FEARLESS BUT NOT MORE RECKLESS!” THAT WAS MY MESSAGE.”

A: I loved that message…yes, dear friend ‘fearless of the opportunities but not reckless’ in 2022!

C: SEVERAL COMMENTS: TALEB’S SKIN IN THE GAME IS A GREAT BOOK!

C: LOVE RAMMSTEIN, HATE THEIR VIDEOS.

A: Agreed (the new ones)

C: JUST THOUGHT I WOULD SAY THANK YOU FOR YOUR OPINIONS! NOT LOVING YOUR RAMSTEIN CHOICE. LOL. BILLY IDOL NEXT ISSUE!

A: Ha-ha, OK, you are not alone. We opted for old style rock n roll today. Good ol Lou Reed.

C: THANKS OZZY, REALLY APPRECIATE ALL YOU GREAT INSIGHTS ON THE MARKETS. ALL THE BEST TO YOU AND YOUR FAMILY.

Q AND C:

READ THIS: Quit fixing things move straight to massive innovation

A LONG BUT REALLY FINE EXCERPT FROM A THOUGHTFUL SUBSCRIBER:

- “…BUT YOU CAN’T TRUST THE GOVERNMENT THEY SAID. AND I DON’T (REVIEW 2000 MULES MOVIE). I DO MY OWN RESEARCH AND WHILE THE GOVERNMENT IS GOOFY AT TIMES, THEY ARE VOTED ON EVERY FEW YEARS. THERE IS A CHECK. THERE IS NO VOTE ON CRYPTOCURRENCIES. I LEARNED LONG AGO THAT UNFAIR AS IT MAY BE, I WOULD RATHER MAKE MY OWN MISTAKES! THE GOAL IS TO FLEECE THE LAMBS, NOT SINK THE SHIP. I HAVE MANY MORE SUCH STORIES.EVERY GREAT BOOM STARTS WITH 1000 COMPANIES WITH A DREAM AND ENDS WITH ONE MARKET LEADER AND TWO COMPETITIORS. THE ODDS ARE NOT GOOD YOU WILL GET THE RIGHT ONE…. IN THE PAST I HAD NOTICED WHENEVER I GET A CLEAR VOTE OF SIMILAR INVESTORS THAT ARE EXCESSIVELY BEARISH OR BULLISH, DO THE OPPOSITE!

A: Thanks for sharing – a lot of wisdom here.

COMMENTS ON 3D PRINTING:

- Hi Ozzie, I came across this article after reading about 3d printing in this month’s OzBuzz. https://www.nelsonstar.com/news/no-hammers-required-kootenay-company-using-3d-printer-to-build-affordable-housing/

- Regarding “printing a 3D house” – I may have mentioned boxabl.com to you before… beautiful application where you can get them (Canada maybe in the next 12 months)

- Every company will be shifting from analog to digital, new blockchain technology, there by switching a million different things like 3-d printing body parts and houses.

Q. I TAKE IT YOU ARE NOT IN CRYPTO?

A: Haha. I wonder why you come to that conclusion. But look I’m concerned nevertheless about all the people that lost their shirt. It is an ENORMOUS OUTLANDISH LOSS! But primarily I am concerned about the impact it will have on all private real estate. Please remember I give no advice…I am opining (if there is such a word).

Think about this: Bitcoin and Ethereum were to be the antidote to the stock market and inflation. “Stick it to the man.” Well, its now clear that Bitcoin travels with the stock markets up and down…like it or not.

Since I expect markets to soften further, I‘d stay away from crypto too. You have to feel sorry for the people of El Salvador. It’s now been proven: High rates are bad for Bitcoin. Crashing Nasdaq is bad for Bitcoin. Fraud and scams hit the middle class like a freight train.

Q: WHAT IS YOUR VIEW ON EVEN HIGHER INTEREST RATES?

A: I feel that if the government stays the course (likely) we may see a .75% increase on July 13. at least though a .50% . What to watch:

Friday the 10th the CPI numbers come out in the US. Consensus forecast is for an 8.2% rate, which pundits will call good. If it is that or below, stocks will rally …for a day. If it is higher, they will fall for much longer.

Q: WHY CAN’T YOU PUBLISH ALWAYS ON THE SAME DAY. IT’S ANNOYING?

A: Wooha! The numbers are produced when THEY are ready. I analyze them and the issues that I have an opinion on when I’m ready. Oh, if I annoy you, please unsubscribe and of course: you get what you pay for.

Q: OZZIE, THE ELITE IN DAVOS MEET AGAIN THIS MONTH TO DISCCUSS THE NEW ENVIRONMENT AGENDA. WILL THEY EVER SOLVE ANY PROBLEMS? LOOKS TO ME THEY CREATE NEW ONES AT EVERY MEETING?

A: 1. Listen to Mike Campbell Money talks (info@mikesmoneytalks.ca) He has a fine editorial on the “Great Reset” Also his guest talks at length about the silly assumptions environmentalists make.

2. Davos conference attendees are not impacted by increases in prices/inflation/wage stagnation/recession. It is always the poor that get creamed in a massive inflation like today.

Q: I LIKED YOUR TRUTHS ITEM. YOU ALWAYS MAINTAINED THAT YOU MAKE THE MOST MONEY ON THE DAY YOU BUY. THAT INCLUDES AN EXIT STRATEGY.

A: Indeed. Plus, URGENT… at this time: Always preserve and protect what you have first. This is more important than ever! Cash is not trash! Revisit my outline on how much cash you should have at a given age.

Q: I SEE HUGE OFFERS RIGHT NOW FROM SOME DEVELOPERS. NOT ONLY 5% DOWN AS YOU SAID, BUT CASH REBATES OF $100,000 ETC. IS THAT A SIGN OF A CHANGING PRE-SALE MARKET?

A: I have not seen such a rebate but yes, a return to a more normal market. Not a weekend blowout but having time to make an informed decision.

Q: YOU SPEND A WHOLE ISSUE SCARING US TO DEATH BUT NOT WHAT WE SHOULD BUY?

A: Actually, I never try to tell you what to buy. I try to give you opinions on issues impacting our investor oriented real estate world The idea is for YOU to make better and your own decisions. If you read the 5 Oz Buzz issues of 2022, the background provided can give you a (totally correct) reflection of market environments. So, read, weep, and decide for yourself.

Q: CONGRATULATIONS, OZZIE. YOU SAID LAST YEAR THAT THERE IS NO TRANSITORY INFLATION. THE PROOF, DEAR SIR IS IN THE OZBUZZ!

A: Ha-ha, thanks!

Q: HOW DOES IT HELP THE FIRST TIME BUYER, IF STRESS TEST IS NOW AT 7%?

A: Well, its actually 6.19% right now (7% to come). But you hit the proverbial nail…It does not help. Look for the “how to beat the stress test.” But wait, the Government will participate in the profit with you – the first-time uneducated buyer – by granting you a mortgage – see below. Yes, you knew it, there is a catch.

Q: LOOKS LIKE YOUR US DOLLAR FORECASTS CAME TRUE. LAST WEEK HOWEVER THE DOLLAR HEADED LOWER. INCREASES OVER?

A: Well, the US dollar hit a 20-year high. Higher? I don’t know. But in my view, it will be higher against all currencies. Other currencies may (decide to?) head lower.

Q: HONG KONG CHINESE ARE LIKELY TO FLEE TO CANADA. WILL THAT HAVE AN IMPACT ON REAL ESTATE IN VANCOUVER?

A: If they have a Canadian passport the can buy anytime. If they “flee” because of Mainland China pressure, they are more likely to go to Singapore, London, and Australia. Oz Buzz wrote about that likelihood last summer. London has open arms; Singapore has better action-oriented business climate and Australia has no foreign buyer’s tax.

Q: ON YOUR ITEM OF TORONTO BEING ON STRIKE, DO YOU EXPECT THE SAME IN VANCOUVER?

A: No, the news has turned, sales are crashing. Workers will become more concerned about still having a job.

Q: I WAS BLOWN AWAY BY YOU TELLING US THAT THERE WERE 18,000 CRYPTO COINS WITH 8000 DEFUNCT. I CAN’T BELIEVE I DID NOT KNOW THIS. I WAS GOING TO IVEST WITH SOME OF THE BIG STARS.

A: Well, they are ‘altcoins,’ but the key is the scams that are being done to unsuspecting you: Movie star creates/promotes (even Matt Damon) frenzy site, public buys, insiders/stars grab all the money, movie star says “sorry.” You are out your money.

Q: I REALLY LIKED YOUR ZOOM MEETING LAST APRIL WHERE YOU SAID THAT 69% OF CANADIANS OWN THEIR OWN HOME. YOU CALLED IT A FABRIC OF OUR SOCIETY. I DIDN’T GET THAT. ALSO WHERE DO YOU GET THE 69% NUMBER?

A: The immigration offices of the world are clogged with people who are dying to get to Canada. Why? Because of our society. Our belief in democracy, our legal systems, safe banks (6 banks versus a 1000 elsewhere). But also because of our system of ownership. We went from 63% to 69% (US is 64%) because we believe in home ownership. It allows us to build equity and leave something for the next generation. It is the very fabric of our ‘owner oriented’ society. That is why we MUST FIGHT every attempt of our government to tax the equity in our homes or paint homeowners as villains, when it is government which under the ‘umbrella of helping affordability’ makes ownership increasingly unaffordable.

The Mag has a great outline on the issue.

MAJOR POINT

When homeownership is attacked by outside influences it does affect us. All people but particularly older people want to keep what they have. All of us feel wealthier with home equity building. We renovate, beautify, and pay off mortgages happily.

When markets go down and homeowners perceive (perceive!) that they lose a big piece of their wealth it affects them negatively. At least for a while. Not feeling wealthy takes buyers out of the real estate market. That’s why we are at a watershed of timing.

Q: HI OZZIE, HAVE LOVED YOUR PERSPECTIVE FOR OVER 25 YEARS. HAVE SOLD REAL ESTATE AT THE HIGHEST LEVEL FOR 16 YEARS, SITTING AT KITCHEN TABLES OF HUNDREDS OF PEOPLE. QUESTION:

DO YOU BELIEVE THE ONLY REAL ANSWER TO THE ASSET INFLATION OF THE LAST 100 YEARS IS THE PRINTING OF MONEY BY EVERY SOVEREIGN NATION ON THIS PLANET? WITHOUT GOING TO THE PRINTING PRESS, AND MAGICALLY FINDING THE MONEY TREE, OUR ASSETS COULDN’T POSSIBLY BE AS HIGH AS THEY ARE?

DO WE JUST CONTINUE TO ASSUME “THEY” WILL ALWAYS PRINT MONEY?

A: The Romans 2000 years ago hollowed out gold coins and put silver in the middle first, then iron! The debasement of money is nothing new. Government will always ‘need’ more money then it can tax.

Today governments of the world owe more money than they will ever be able to repay. Nay impossible to repay….so they will continue to create money out of thin air. I have for that same 25 years repeated my belief that “inflation is primarily a monetary phenomenon (Milton Friedman). I still belief that. However, I also have my 4 pillars of equal importance. The second pillar of timing we have now entered. Anyone studying the numbers can see it happening as we speak. Get safe!

Q: IF REAL ESTATE PRICES IN VANCOUVER CONTINUE TO RISE DUE TO INFLATION AND WAGES ARE NOT RISING TO THE SAME DEGREE, HOW DO INDIVIDUALS CARRY THE EVER-INCREASING MORTGAGE DEBTS? I HAVE A FEW FRIENDS THAT HAVE MORTGAGES OVER $1MM AND HAVE NO CONCERNS ABOUT THEIR ABILITY TO EVER PAY IT OFF. FOR EXAMPLE, A HOUSE IN THE WEST SIDE FOR $4.4M, WHERE DOES SOMEONE GET THE $1.1MM (25% DOWNPAYMENT) AND THEN SERVICE A $3.3MM MORTGAGE WITH MONTHLY PAYMENTS OF ABOUT $15K PER MONTH. HOW DOES THE AVERAGE VANCOUVER FAMILY PAY THAT IF AVERAGE FAMILY INCOME IS $60,000 PER YEAR? I UNDERSTAND THAT HARD ASSETS INCREASE IN VALUE DUE TO INFLATION, THE DEBT SERVICE SIDE IS NEVER MENTIONED.

A: Your statement is correct. But it is NOT a question of affordability, Vancouver has not been affordable for 40 years. If you want to live in Hong Kong, London, New York or Vancouver you must have the kind of income you don’t earn here. Also, yes: If the average mortgage is over $800,000 then in a downturn, we will see more defaults.

BOOK OF THE MONTH

Everything Is F*cked: A Book About Hope, Mark Manson. We live in an interesting time. Materially, everything is the best it’s ever been—we are freer, healthier, and wealthier than any people in human history. Yet somehow everything seems to be irreparably and horribly f*cked—the planet is warming, governments are failing, economies are collapsing, and everyone is perpetually offended on Twitter. At this moment in history, when we have access to technology, education, and communication our ancestors couldn’t even dream of, so many of us come back to an overriding feeling of hopelessness. What’s going on?

Everything Is F*cked: A Book About Hope, Mark Manson. We live in an interesting time. Materially, everything is the best it’s ever been—we are freer, healthier, and wealthier than any people in human history. Yet somehow everything seems to be irreparably and horribly f*cked—the planet is warming, governments are failing, economies are collapsing, and everyone is perpetually offended on Twitter. At this moment in history, when we have access to technology, education, and communication our ancestors couldn’t even dream of, so many of us come back to an overriding feeling of hopelessness. What’s going on?

This book will rattle your cage. Yep, your cage! I get his weekly irreverent treatise, not in agreement often, but given to thoughts.

TOILETS OF THE WORLD

NOW why a fish tank there? Why not?

SONG/MUSIC OF THE WEEK

So many notes on my song of the week. Actually, several wonder, why do it at all? Ha-ha, if you want to be eclectic, you have to be, well eclectic.

Rammstein had some surprising responses, with many older songs recommended by several, but more “why” comments. This week these golden oldies:

Lou Reed and David Bowie

WAITING FOR THE MAN https://www.youtube.com/watch?v=W4VEXl4vsq4

Just a perfect day https://www.youtube.com/watch?v=uCpkwAkNJj0

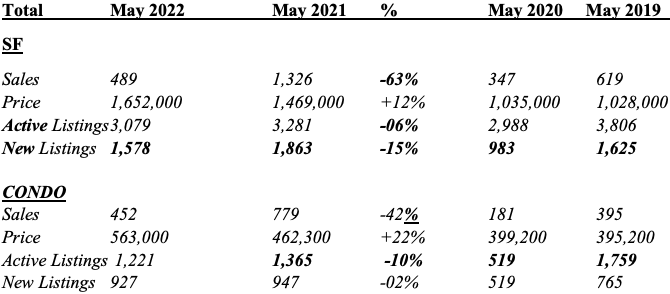

THE NUMBERS: TORONTO, VANCOUVER & FRASER VALLEY

TORONTO The final numbers were not released at time of this issue. Average sales price year over year is still up 9% but only 9%! Prices on average are down 3% April over May and sales are down 38%.

VANCOUVER

Again: Remember to take the 2020 comparisons with a grain of COVID salt! Snapshot:

SF: The Real Estate Board of Greater Vancouver (REBGV) reported SF sales of 967 in April 2022, a 42(!)% decrease. May came down by 44%! Fewer single-family homes sold than even in 2019. The average price achieved in April of $2,312,000 is down by $110,000.

CONDO: REBGV reports condo sales down 21% over May 2021 sales. The condo average price is only down $22,000 from April. Condo new listings are down (only) 9% over last May but well UP over 2019.

- This is the Vancouver average. Some areas are down further, some not. North Vancouver for instance is not as dramatic since the SF Price high was in March 2022 (5 year high) at $2,417,000 then

April 2022 at $2,391,000

May 2022 at $2,368,000

Not dramatic and only 3 months – but the trend is down when you add sales: - Sales: High was

April 2021 183

March 2022 117

April 2022 96 - It really is interesting when you look at properties over 2,600 sq feet and over 4 bedrooms:

In that subsection March 2021 clocked in at the absolute high in sales for proprieties over 2,600 sq feet and over 4 bedrooms: March 2021 = 88, May 2022 = 29.

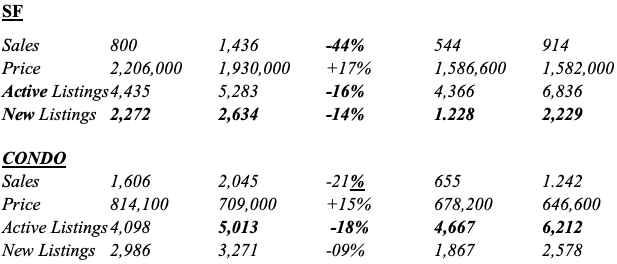

FRASER VALLEY

Heard at a UDI meeting (Ferreira):

Surrey has been a Pandemic winner. SE Asian community went behind every project because they believed in Surrey. Many reasons: New city centre, UBC made a huge investment close to hospital, which helped buyer confidence.

Recently as wood frame building was launched at $920 a foot and Highrise are now over $1,100. What was TH at $600,000 is now $1.1 million.

Agreed. Certainly, my partner Ralph Case and I have promoted Surrey and bought and sold there for years.

However, this was a strange month in the Valley; SF home sales CRASHED by 63%. The average price (declining every month since February) cracked from $1,929,000 in February 2022 to $1,652,000 in May – a 15% drop. Active SF listings are lower than May but 800 listings HIGHER than in 2019.

Condominium sales cracked as well, down 42%. New listings are higher by 15% than 2019 – still down 2% over last year.

Fraser Valley

- February SF sales were down a whopping 37%

- March down by 33%.

- APRIL? Down 56%!!

- May 63%!!!

- Condominium sales are down 20%.

- NOTE: SF Prices are still up by 18% but $170,000 down over February’s $1.9 million

- February: $1,928,000, March $1,818,000, April $1,757,000, May $1,625,000

OWNERS SHARPEN PENCILS?

MAJOR, MAJOR POINT: As we said on February 9: THE HIGH IS IN PLACE. For the last three months we pointed to a changing market … before the interest changes and the stock market and crypto crashes. Now, the fast increase in rates really starts to bite. We expect that to continue and even accelerate into the summer. If we are right and July may actually see a .75% increase … all bets are off.

Ozzie, Michael Campbell, Michael Levy and Victor Adair and guests are now on podcasts every week: https://omny.fm/shows/money-talks-with-michael-campbell

- If you are in building, selling, marketing, developing, lawyering, etc. list yourself in the free BC real estate directory: www.bcred.ca

- Questions to Ozzie and experts: www.askanexpert.ca

- Set up your own “talk” at www.realestatetalks.com . Ozzie’s 24-year-old bulletin board for you to play in.

- Want to see all Ozzie blogs and all Ozzie podcasts? Go here: www.ozbuzz.ca

- Who the heck is Ozzie? Go to www.ozziejurock.com.

- Ozzie on YouTube? www.youtube.com/jurockvideo

Oz Buzz Podcast

Disclaimer

Subscribe

| Subscribe to Oz Buzz: |

(You’ll get Oz Buzz 2 weeks before it’s posted online)

Leave A Comment