“A boom creates money raining on fools”

Where Mike, Gordon, Ozzie, and the MoneyTalks Gang did the Polar Bear plunge. Or did they cheat?

March 9, 2023

AGENDA

- THE WORLD, OUR WORLD, ECONOMY, INFLATION, RECESSION

- WHERE LAWYERS ARE SMILING

- THE GREAT RESET! WHAT? READ IT AND WEEP!

- QUESTIONS, QUESTIONS

- 4.7% 5-YEAR TERM IS A GOOD RATE

- MAJOR US MORTGAGE DEFAULTS ON $1.7 BILLION

- LISTEN TO PODCASTS

- INTERESTED TO JOIN THE REAL ESTATE ACTION GROUP IN VANCOUVER? COME AS OZZIE GUEST – CHECK IT OUT.

THE WORLD, OUR WORLD, ECONOMY, INFLATION, RECESSION

EUROPE INFLATION AND RATES

Annual inflation across the 20 countries stood at 8.5% in February (EU’s statistics agency). Worse, inflation ticked up to 9.3% in Germany, Europe’s largest economy. It also rose in France to 7.2% and in Spain, to 6.1%.

The so-called “core” inflation number that strips out volatile food and energy prices, jumped to 5.6% from 5.3% in the eurozone. The risk that inflation is becoming embedded more deeply across the European economy is now very high.

Feb 28 (Reuters) – Home prices in Germany, Europe’s biggest economy are forecast to decline 6.8% this according to a Feb. 27 poll.

Major Point: With the ECB expected to hike interest rates at least twice more in coming months and inflation still running around 9%, that trend is unlikely to reverse soon. The same holds true in all European real estate markets.

US INFLATION, INTEREST RATES, DOLLAR, AND MORTGAGE DEFAULT

Fed Chairman Powell testified before the US Senate on March 7. He quickly sent all the markets into decline (Dow fell 575 points) when he mentioned “if the totality of the data were to indicate faster tightening is warranted, we would be prepared to increase the pace of rate hikes”. On March 9 the weekly report on initial filings for unemployment insurance showed 211,000 claims, an increase of 21,000 from the prior week. Even so, markets kept declining. The consensus is now for a 50 BP hike on March 22. US inflation is still over 8.2%. Time will tell. In any case rates will NOT come down.

US MORTGAGE

The average rate on the 30-year fixed mortgage jumped back over 7% rising to 7.1%, according to Mortgage News Daily. Mortgage rates follow the yield on the U.S. 10-year Treasury. In Canada long term rates (5 year) are tied to the bond market as well.

USA: Huge Landlord Defaults On $1.7 Billon.

CMBS Mortgage & Banks Lose Billions. These kinds of defaults will continue. This is why even for the smaller investor I urged you for several months to consider redeeming your investment. Not that it is necessarily bad, but with many of the investors wanting out … you may not see your money for years – if ever. We talked about all funds – including some REITs, MICs small private funds etc. We also talked about the world’s biggest fund manager Blackrock, 2 months ago. In November redemptions in Blackrock’s REIT hit $1.7 billion!! Since then, Blackrock redemptions hit every monthly limit again, billions!

Major Point: We are in the middle (still) of a monetary crisis. Liquidity and falling asset prices crunch the ability of funds to redeem its shareholders since most funds are invested in fixed real estate assets that are not easy to sell in this market. Stand on the sidelines – we said – with your cash.

CRASH

Open-Door, Zillow and others went into the single-family home market like spoiled children. Paying any price to get into the business. Now they are paying a big price to get out. As we said in the November Ozbuzz … Investors now go to the city they like and find out whether Blackrock, Zillow or Open-Door owns houses there and then … stink bid time.

CANADA INFLATION, CANADA INTEREST RATES

We were told by the BOC that the January rate increase would be the last time for awhile in Canada. That is why it was very unlikely that the March 8 rate announcement would be a raise. In fact, the BOC did announce that it will not increase their overnight rate – risking accelerating inflation. We said in previous Ozbuzz’ that they would likely pause, but NOT go down for some time.

Note: This is the first interest rate pause of the previous 9 meetings. However, the bank will continue to monitor inflation and “…we will not be afraid to increase rates yet again”. Canada’s economy has stalled to 0% growth (the BOC desired outcome).

However, the FED later this month will raise another .50% (at least .25%). If that continues, the Canadian dollar will crash further and the BOC may have to act sooner. The next announcement will take place April 12th. The Canadian Dollar remains oil dependent. You make the call: Oil higher or lower?

Current best rates by Kyle@GreenMortgageTeam.ca:

1yr. 5.79%, 2yr. 5.49%, 3yr. 5.25%, 4yr. 5.19%, 5yr. 5.14%

Variable: Prime -.8% = 5.9%

Insured

5yr fixed: 4.79%

Variable: Prime -1.1% = 5.6%

Aways check your best rate with a professional broker.

Major, Major Point: The biggest wisdom on the likely outcome: The maddening: IT DEPENDS!

Global liquidity crisis pending… if new money creation slows down, a collapse in financial markets could spill over. Some call such a collapse a necessary detox cleanse.

We still believe that we will muddle through and higher prices (inflation of hard assets) will be the eventual outcome. Question is when? We believe it will take all of 2023 and then some to work out a bottom.

The interesting thought: Inflation today comes from the supply side (too much money printing) not the demand side … yet the FED/BOC/ECB act as if we have a demand side problem … thus – in their view – rates must get higher from current levels. However, debt also continues to increase. As debt increases and higher rate defaults happen, more liquidity crises (private and governments) indeed will happen worldwide.

US dollar: As we speculated in past issues. Higher rates mean money from around the world will flee into the US dollar – safety and better return. Rather than staying in their own countries… Thus, yes … US dollar increases and other countries currency decrease. The intent? To kill inflation is to have a global slowdown. Result? A worse global debt crisis with rising dollar.

Dear Reader: No one knows. The outcome is NOT certain. I believe that higher inflation in 2 – 3 years will feature higher prices again. Convinced. But unless we know for sure… On the sidelines with cash remains a good thing!

The fine newsletter “Trend Letter” info@thetrendletter.com (subscribe) POSTED a fine summary of the stock market last month:

QUESTIONS / COMMENT ON ‘THE GREAT RESET’

I continue to be asked about the German Klaus Schwab and his New World Agenda or the Great Reset. Conspiracy theory or? Well, the meetings in Davos at the World Economic Forum prove it constantly. It is no conspiracy theory – it is a factual living plan. The ‘elite’ plans to do away with much of the population (you and me), all of the financial and legal institutions and to replace it and them with a NEW world order.

New World Order Agenda:

1st step is planned destabilization (we have gone through it)

2nd step is deconstruction (we are in it)

3rd step Re-construction – new financial system (Those that try to kill us will want to emerge as saviours.)

Final result: Control of all resources and systems – after the GREAT RESET. They are not acting negligently they are acting on purpose. They want population control!

Not a good quality video but a fine summary of the New World Agenda

Major Point: Take a minute watch/listen to the video. Inform yourself. I welcome your opinions.

“A recession is not necessarily a bad thing, you need an economy enema.” –Elon Musk

FOREIGN BUYER BAN

Unintended consequences require amending SAYS Benjamin Tal.

In a wide-ranging treatise of the new Foreign Buyer prohibition Tal goes after the government in an accurate relentless way. While the motivation is to improve affordability by reducing a source of demand, foreigners consists of a very small percentage of the market anyway. 2.2% in Ontario and 3.1% in British Columbia.

Government seems to think there is nothing to lose. Tal argues that there is plenty to lose. He quips: “The language of the Act appears straightforward until you show it to a lawyer!” (lawyers are smiling)!

Ambiguous terms like “residential property” mean what? Detached, semi-detached, condos. Ok, but also any developed or vacant land that does not contain any habitable dwelling and that is zoned for residential or mixed use and also is located within a census metropolitan area! What’s it mean when census area would be all of downtown Toronto? Oh, not to forget the many commercial real estate assets that happen to be on land with zoning that permits a residential. Oh, and farmland within a census metropolitan area?

Confusing for you? Ok, but what exactly is “non-Canadian”? Yes, could be REITs. In fact, based on the language of the Act, the vast majority of publicly traded Canadian REITs are foreign entities. There is more – much more. Tal says: “Policymakers should immediately take another look and amend the Act in a way that is consistent with what it was intended to achieve.” Here, here! We are with you Mr. Tal.

Major Point: Read it and weep!

QUESTIONS, QUESTIONS

Q: I am concerned about a banking default. Can Canadian banks close their doors and not give me access to my money? Happened in the US in the past and is happening around the world now.

A: 5 Canadian banks have 5,701 branches. In the US they have (previous defaults) 5,000 banks with 1 branch. One branch can easily default. Not the massive Canadian banks!

Q: All the mortgages, all the bond debt, corporate debt and government debt will be rolled over (on term expiry) at higher rates. Where to be safe?

A: Some will not survive the increases. Most will. YOU? Be in cash until the smog lifts.

Q: Thanks for your Oldfluencers. Now at least I have a name I can call mine! When I saw the first OldF…I thought it would be Old Fart.

A: Ye, of little faith. Go and now oldfluence with your money, your buying power.

Q: I hear there are multiple offers. Is the market changing?

A: Multiple offers on best priced properties under $1 million price range I heard about too. But reality is, that mortgage brokers tell me: “…it is much harder to get the application” over the line ”or funds were withdrawn at the last minute”, or client file is waiting 7 weeks for approval. Realtors tell me, I have 8 deals, but only 2 will close for sure (financing other subjects uncertain). Buyers spook easily. Very, very few multiple offers.

Q: I think you don’t need Kudos. Your head is big enough.

A: Ouch

Q: On your things that annoy me. OMG, I thought I was the only one that hates self-checkout and that no one will bag your stuff anymore. Maybe make a list of stores that do pack and those that do not? Revenge of the little man?

A: Ha-ha. Revenge of the little man (ROTLM) with a target, OK. I bite. I live downtown close to Safeway. It’s convenient and free parking. But they purposefully throw my foods to the end of the counter (out of the cashiers reach and a bag on top). Then stare you down. You have no choice but to pack it yourself. ROTLM? We drive to IGA … not only do they pack it, smile while they do it and the paper bags have handles on it (Urban Fair too) ROTLM – yeah!

Q: Do you use ChatGtp writing your Oz buzz? Do you use .ai to create your videos?

A: No, I do not use Chatgtp.ai for Ozbuzz. It uses the average of hundreds of possible answers to create its blurbs. I want to be unique. However, I do use pictury to create videos.

Q: I like you, but your numbers conflict with the numbers put out by the real estate board.

A: All my numbers come from all the boards. Nowhere else. The boards put out the best numbers. Average price, median price, benchmark price, seasonal adj price etc. But you have to pick the right ones for your purpose. I like to pick the averages – because they were actual deals done in an actual month.

A great example of confusing is this week’s posting of transactions from the Toronto Real Estate Board

1. Action sales Feb 2022 = 9,028. Actual numbers of sales Feb 2023 = 4,783 – DOWN = 47%

2. Season adjust Jan 2023 =4,814. Seasonal adjusted Feb 2023 = 5,224 UP + 8.5%

If you see number 2 all is well, even downright good. UP 8.5%

If you see number 1 all is bad, very bad. Down 47%.

To compare these side by side is ridiculous until you also quote January 2022 versus Feb 2022.

Things to do:

Look for assignments in Craigslist, Kijiji etc. Attend presale lunches.

Join the Real Estate Action Group meetings in Vancouver.

Come as my guest one time (must be booked ahead of time)

Next Monday March 13, 2023 – 6:30PM.

TOILETS OF THE WORLD

Team building…?

THE NUMBERS, THE NUMBERS

TORONTO

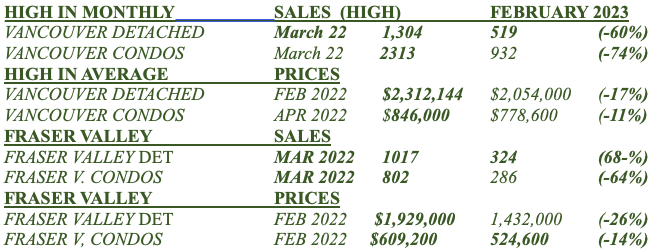

Toronto Market High of 2022 versus Feb 2023

Ok, you say…you are comparing wrong numbers. No, I compare the highs of 2022 to today. By end of March – everyone will!

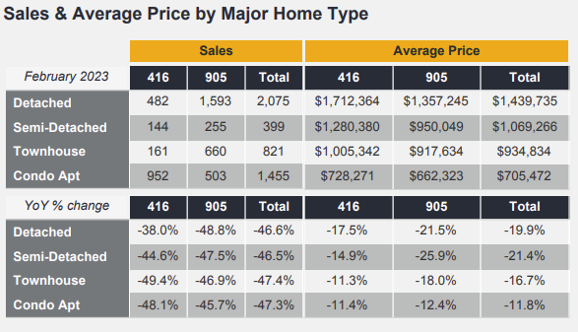

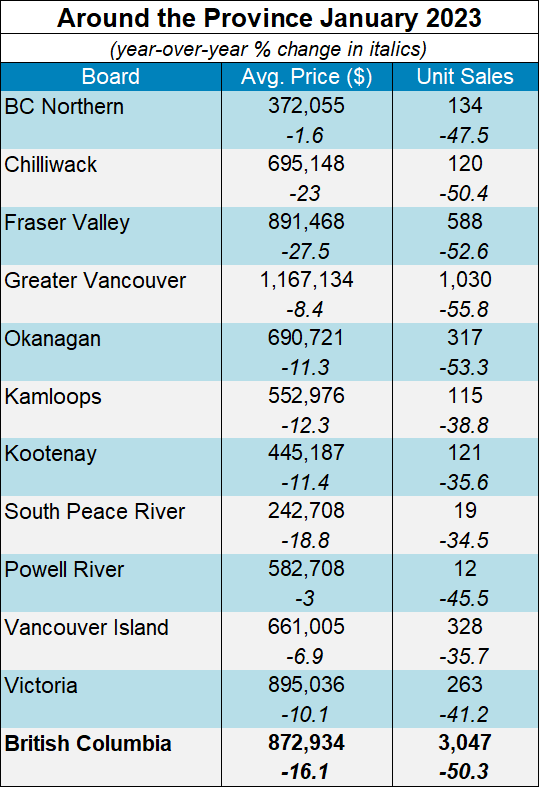

BRITISH COLUMBIA (February as of March 9 not published yet)

For the ‘real market conditions’ we show the 2022 HIGHEST MONTH (first).

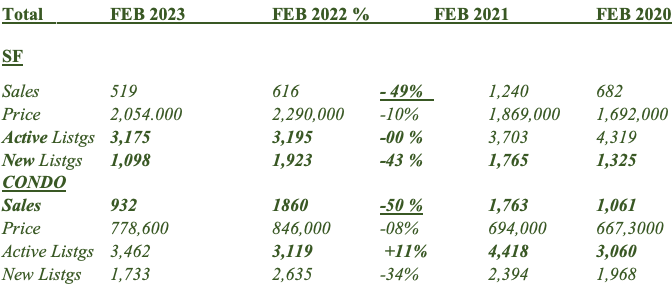

VANCOUVER

Snapshot:

SF: REBGV reported SF sales declined a further 49% over FEBRUARY 2022. The average price high achieved in April of $2,312,000 is down by $258,000 – or 11%.

CONDO: REBGV reports condominium sales are down 50% over FEBRUARY 2022 sales. The condominium average price is down by 10% from April 2022.

- Then note the 4-year comparisons – high in everything for the last 4 years was March 2021.

- Major Point: Note the downturn from the high in the opening. Then note increase in active listings – up 15 %/14% for condos and SF. Active listings are way up in VF (condos up 136%!)

- New listings might be down but active listings are way up. If you add them together and compare to 2022 – we are higher.

- Study the above at the opening comparison of the ‘high in sales’ (usually FEB/APRIL) and the high in Vancouver prices (usually February 2022) and note the sharp declines in all sales and continued declines in all prices.

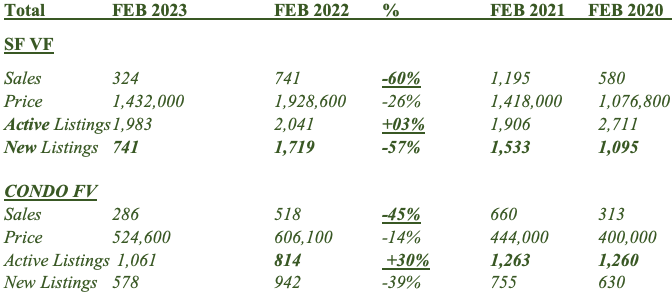

FRASER VALLEY

SF home sales continued their sharp downturn (-60%). Prices are 30% lower. Active SF listings (+49%!) as well as condominium listings are up a whopping +112%! Condominium sales cracked as well, down 52%.

The numbers tell the story. Look at intro to the numbers and the comparison of February 2022 to FEBRUARY 2023, still a 26% decline in single family home prices, 14% down in condominiums. A tad better than December’s prices.

REMEMBER THIS:

Aldous Huxley:

“There is only one corner of the universe you can be certain of improving, and that’s your own self.”

Subscribe

| Subscribe to Oz Buzz: |

(You’ll get Oz Buzz 2 weeks before it’s posted online)

Well done , we all need to hear this