“He has all the virtues I dislike and none of the vices I admire.”

April 8, 2023

AGENDA

- THE NUMBERS BETTER IN MARCH

- FOREIGN BUYER BAN CHANGED

- UNUSED HOME TAX MAY APPLY TO YOU TOO

- BC LAUNCHES NEW HOUSING INITIATIVE

- BC THREATENS FLIPPERS BUT OFFERS $40,000 FOR YOU TO FIX YOUR BASEMENT

- BASEMENT SUITES LEGAL IN THE WHOLE PROVINCE

- INFLATION/ DEFLATION

- QUESTIONS, QUESTIONS

- 5-YEAR TERM IS HIGHER – BUT BEARABLE

- AS PREDICTED (SOME) MAJOR CANADIAN REITS HALT REDEMPTIONS

- WE SAID IT: THE DOLLAR – OIL DEPENDENT AND THEN SOME

- FEARLESS FORECASTS

THE WORLD, OUR WORLD, ECONOMY, INFLATION, RECESSION

EUROPE INFLATION CONTINUES

The euro area annual inflation rate was 8.5% in February 2023, down from 8.6% in January. A year earlier, the rate was 5.9%. European Union annual inflation was 9.9% in February 2023, down from 10.0% in January. England and Germany are double digits.

Major Point: No surprise. With these high rates the ECB hiked interest rates a full half of one percent. We predicted it and predict more to come. We said: “… that trend is unlikely to reverse soon. The same holds true in all European interest rate decisions and affects all European real estate markets.”

USA

US INFLATION, INTEREST RATES, DOLLAR, BANK DEFAULTS

Much has been reported about the SVL and Credit Suisse bank collapses. We don’t wish to beat a dead horse. We are indeed not out of the proverbial woods yet. Clearly, our multi-month admonition of “4 ugly months ahead” and get into some cash was well forecast.

We discussed last month the continued stress on the US real estate market (particularly commercial and office), the reported $1.7 billion mortgage crash (one company!) and house flipping companies at length in the last issue. Almost like foresight! We also salute the subscribers who went and bought Zillow, Opendoor and Blackrock aggregator real estate at a 30% plus discount!

Freddie Mac says in the April 2023 primary mortgage market survey that the 30-year-fixed-rate mortgage is down to 6.28% – best in 6 months. The 15-year fixed-rate mortgage averaged 5.64 percent.

According to Redfin, U.S. house hunters are beginning to ‘wade into the market’ in bigger numbers as mortgage rates and home prices continue to decline in late March 2023.

Low supply is the biggest problem reported. There is more optimism in the residential market. Decline of prices are much lower than in Canada.

For instance, Las Vegas Realtors report that the median price of a SF home during March 2023 was $425,000. That’s almost identical to the previous month and down 7.6% from $460,000 in March of 2022. It’s also down from the all-time record price of $482,000 in May of 2022.

The median price of local condos was $260,000. That’s down 3.7% from $270,000 in March of 2022. It’s also down from the all-time record price of $285,000 in May.

Major Point: Yes, to the bigger questions: Will we muddle through? Our answer remains, yes, we always have and we always will. But it isn’t over yet.

LAYOFFS CONTINUE IN THE US

- Planned layoffs totaled 89,703 for the period, an increase of 15% from February, according to Challenger, Gray & Christmas.

- Job cuts have soared to 270,416 so far in 2023, an increase of 396% from the same period a year ago.

- The damage was especially bad in tech, which has announced 102,391 cuts so far in 2023. That’s a staggering increase of 38,487% from a year ago.

Major Point: Layoffs continue but overall employment is still strong. But these are lagging indicators. Stay on the sidelines till the fog of confusion clears.

US DOLLAR

We speculated last month: “Higher rates mean money from around the world will flee into the US dollar – safety and better return. Rather than staying in their own countries… Thus, yes…US dollar increases and other countries CURRENCIES decrease.” The ‘fleeing for safety‘ statement is still valid… But we also said: “No one knows. The outcome is NOT certain.” We still say that. Also, please go to questions and note that India is trading in Rupee WITH 18 NATIONS!

Clever quips:

“I am enclosing two tickets to the first night of my new play; bring a friend, if you have one.” –George Bernard Shaw to Winston Churchill

“Cannot possibly attend first night, will attend second… if there is one.” –Winston Churchill, in response.

CANADA

INFLATION CANADA INTEREST RATES

The annual inflation rate in Canada reportedly fell to 5.2% in February slowing from the 5.9% in the previous month. Inflation for shelter 6.1% vs 6.6%, food costs 9.7% remained high. We think our inflation is actually higher, dramatically so in larger cities versus smaller cities. Rents are well up over 10% in TO and Vancouver, etc. Our early departure from rate increases and our crazy government overspending will keep rates high. (Numbers from Statistics Canada.)

The Canadian economy added more jobs than expected in March and the unemployment rate remained near a record low for a fourth straight month. Data on Thursday showed, a sign of economic resilience ahead of a central bank policy meeting next week (April 12). The economy gained a net 34,700 jobs, almost entirely in the private sector, and the unemployment rate held steady at 5.0 per cent. Bank crisis not withstanding the bank may stay put or .25%.

CURRENT BEST (Canadian) MORTGAGE RATES (April 8).

Rates are up a tad. Current best rates by Kyle@GreenMortgageTeam.ca:

1yr. 5.79%, 2yr. 5.29%, 3yr. 4.99%, 4yr. 4.89%, 5yr. 4.6%

Variable.

Prime -.8% = 5.9%

Insured are:

3yr 4.84%

4yr 4.64%

5yr 4.39%

Variable prime -1% = 5.7%

Major Point: Aways check your best rate with a professional broker! Get a quote from Kyle Green: Kyle@GreenMortgageTeam.ca

CANADIAN DOLLAR

We felt that if you have US investments in US dollars that you are contemplating bringing back into Canadian – take a close look. We felt last month that if the Canadian trades in the 72/73 cent range, it maybe a good time to convert and take some ‘US dollar chips’ off the table. Commodity dependent (particularly OIL) our dollar travels as they will. So, to repeat: “The Canadian Dollar remains oil dependent. You make the call: Oil higher or lower?”.

DOUBLE SURPRISE: 1. The surprise shock of dropping production by a million barrels a day (OPEC) this week, saw the dollar briefly hit 74.8 cents. 2. The sanctioned country (Russia) working with the supply country (Saudi) to drop production. (This is payback against Biden, who in a bid to win the mid-term elections, made promises to Saudi Arabia and then welched on them.)

TORONTO OFFICES GETTING EMPTIER

Looks like employees want to stay working from home! CBRE says that the office buildings vacancy rate hit 15 per cent in the first quarter of 2023, the highest it has been since 1995. In suburban Toronto, the vacancy rate was even higher hitting 20 per cent. Not to be gloomy but experts say it will not reverse soon. We like being at home too much.

Major Point: See below Office REITs woes. Rising vacancy rates and higher financing costs are two freight trains heading to a crash.

TWO CANADIAN OFFICE REITS SLASH PAYOUTS

Yes, we said: Be cautious if invested in MICs, REITs, private funds and particularly funds invested in commercial and office real estate. You may not be able to redeem – for months – even years, we said. We told you to take your investments out last fall and then again, this January/Feb/March. Get the cash. It’s not trash. We also discussed last fall the fact that (mega) Blackrock was halting redemptions. Now Blackrock has halted redemptions on more RE funds and reportedly took a loan (interest rate in double digits) to buy back some (Note: Rumour).

This week two large Canadian REITS slashed payouts. This is spreading gloom throughout the sector. Which funds?

- Slate Office REIT SOT-UN-T is slashing its monthly distribution by 70 per cent, making it Canada’s second publicly traded office building owner to cut its payout in the span of three weeks as vacancies rise and higher interest rates bite. Slate, which owns office properties in Canada and the United States (mostly in the GTA), slashed its distribution to 1 cent per unit monthly from 3.3 cents after a strategic review. Slate’s units now are down 43 per cent this year.

- True North Commercial REIT TNT-UN-T, which owns office properties across Canada (focus Ontario), slashed its own distribution by 50 per cent. True North’s unit price also crashed; its units are now down 45 per cent this year.

Question: Who is next? Like homeowners, REITs usually only face higher rates when their mortgages need to be renewed. But some, such as Slate, chose/preferred variable-rate mortgages. The current market rate for a five-year commercial mortgage is around 5.5 per cent up considerably from last year (about 3%). Plus, office property owners are struggling to keep tenants because working from home has become more common. Slate’s occupancy was 81 per cent when the REIT last reported earnings in February(!).

Slate and True North aren’t the only REITs that have cut their distributions since the pandemic erupted. During the first and second lockdowns, a slew of REITs, including RioCan and First Capital, slashed their own distributions…fearing the markets. Even Allied Properties REIT AP-UN-T, units are now down 62 per cent from their record high set in February 2020. (Allied conference call April 27!!?), then there is Romspen, etc. Enough said.

MAJOR POINT: Dear Real Estate investor our constant urging of getting into (some) cash – citing market related and age-related reasons … is paying dividends. Consider getting 5.2 percent on your GICs for now and sit out the struggle. REITS used to pay that … now no more. Finally, we hear of a number of multi-family buildings also struggling with the higher interest rates.

CANADIAN FOREIGN LEGISLATION BUYERS’ DILEMMA

Last month we quoted Mr. Tal excellent summary of why “amendments are needed”. This month the Federal Government made an about face. The idea of the ban was to stop prices rising. Blaming foreigners, even though they were less than 2 percent of the market and then only in big markets.

So, in a market that saw price declines of 18% – 29% and sales declines 40% to 50%, we took willing buyers out of the market and stopped developers – developing.

Now it seems that the government understood and it amended the foreign buyer ban law because it added and then created problems. Fallout from the legislation was abrupt. Developments that had a small fraction of foreign ownership or were zoned for mixed-use, were suddenly sidelined because of the narrow parameters of the crazy policy.

So, this week there were changes:

A) The prohibition no longer applies to vacant land. It used to be all land now only developed residential property land.

B) Work permit holders while in Canada can buy. Work permit holders are eligible if they have 183 days or more of validity remaining on their work permit or work authorization at the time of purchase.

C) Foreign corporate holding threshold increased from 3% to 10% ownership of a corp.

D) Big change: Development residential purpose purchases are allowed.

The Govt. realized that hundreds of developments were stopped and did something. Good.

But investors are still out. Particularly in the condo market. That’s where a lot of the foreign buyers predominantly would be buying— investment properties, condos. So, that’s why on a lot of developments, developers have pulled the plug on developments.

Major Point: And typically, it was the smaller condo investors. Foreigners don’t buy (resale) homes. It’s really a tiny, tiny percentage. It was pre-sales that get hurt. A developer needs 60% of its units pre-sold before they get financing. Most do not have $80 million laying around and need the financing. No foreign or other investor buying, no building new units, no condos ready for rental when finished.

Conclusion: So new construction suffers… while prices are down 18% – 29% across and sales crashed – we are telling buyers not to invest. It is not the foreign buyer, but incessant lowering of rates that spiralled the market – not the foreign buyer. Now we followed it up with fast crazy high interest rates.

ANOTHER MAD NEW TAX. THE UHT! THE WHAT?

It compels foreign property owners to pay a 1 per cent annual tax on the value of any residential property deemed “underused” or “vacant” by CRA. Started Jan 1, 2023. It was launched with few details – other than threatening steep penalties, but no one understood it.

There was such an outcry that CRA was forced to say last week: “The Canada Revenue Agency (CRA) understands that there are unique challenges for affected owners in the first year of the Underused Housing Tax Act (UHTA) administration. To provide more time for affected owners to take necessary actions to comply, there is transitional relief to affected owners.”

The application of penalties and interest under the UHTA for the 2022 calendar year will be waived for any late-filed underused housing tax (UHT) return and for any late-paid UHT payable, provided the return is filed or the UHT is paid by October 31, 2023.

This transitional relief means that although the deadline for filing the UHT return and paying the UHT payable is still April 30, 2023, no penalties or interest will be applied for UHT returns and payments that the CRA receives before November 1, 2023.

My American/Canadian client writes (T.M.)

“Hey Ozzie – I hope you’re doing great, I’m sure you are. Why would anyone want to own real estate in Canada, especially as an investor?

I just found out we must fill in some new Gov of CA form – Total crap! 6 pages of confusion!

Not simple… just wow!”

MAJOR POINT:

What you may not know CANADIANS MAY ALSO BE AFFECTED! If you hold a property in trust, partnership etc., etc. you may have to pay or even you may not have to pay but you must file. It’s complicated. Go here for details and rant, yell, and cry: https://www.cpacanada.ca/en/news/canada/underused-housing-tax

EBY LAUNCHES A NEW HOUSING INITIATIVE

The British Columbia government will invest billions of dollars in “Homes for People plan”. How much?

- $4-billion investment over three years

- $12 billion over a decade.

They are planning:

- incentives to build and increase density

- more housing for those who are homeless

- zoning changes that make basement suites legal across the province

- crackdown on house flippers – a new flipping tax

Key. It ain’t here yet: Government will introduce legislation this fall to allow:

- three to four homes on a traditional single-family detached lot

- with additional density permitted in areas well served by transit

This hopefully means no more long zoning processes just:

- to build a duplex

- a triplex or

- row homes

Additional legislation will be introduced this year to allow secondary suites in every community across the province, something normally left up to the municipalities.

Homeowners will be able to access a forgivable loan of 50 per cent of the cost of basement suite renovations, up to a maximum of $40,000 over five years. Catch: But they’ll have to rent those suites at below market rates for at least five years. The pilot program is expected to be open next year to at least 3,000 homeowners for the first three years.

Promise also to: … beef up enforcement of short-term rentals and modernize the building permit process speed up approvals.

Major Point: Industry says: we need to see details! What does it mean for local governments by laws, their planning process etc.? How to roll out a seemingly blanket policy.

Major Point: We all want more housing, less regulations and stop the crazy new tax increases. We have heard promise after promise by all handwringing governments. We have been thrown a bone. Let’s hope there will be some meat on it.

QUESTIONS, QUESTIONS

Q: ‘THE GREAT RESET’ GENERATED THE LARGEST RESPONSE TO ANY ITEM WE FEATURED BEFORE.

A: I was bombarded with ‘better videos,’ articles and opinions. Hey, I write a Real Estate Newsletter and stuff that maybe of interest. The interest here is that private ownership is on the table in the reset as in – under attack. That’s why we featured it. Biggest surprise to me? How many of you are well informed and engaged. The world is safe.

Q: YOUR REVENGE ITEM (ROTLM) I GENERALLY LIKE. BUT YOU DON’T LIKE SELF CHECKOUTS AND SOMEONE BAGGING YOUR STUFF? COME ON OZZIE, YOU ARE GETTING OLD.

A: Hm, ok. Maybe. The world is changing, so change with it. But most of these jobs will disappear. (Walmart will be totally automated by 2026 – totally!) There will be no one to talk to about anything. Today try and speak to the same person twice at Shaw or other national companies. Try and get a mortgage payout. You are now a file or a case, which can be handled by anyone here or in India. We are being trained like monkeys. It annoys me that the checkout person that is still there forces you to bag your own stuff by staring you down. Getting old or not … I’ll shop at IGA and even Whole Foods… Get my bag bagged, helpful check out … hey and my paper bags have handles there.

Q: I notice you use a lot of AI in your videos. Do you use ChatGTP?

A: No, I use AI video creation but not ChatGpt for videos.

Q: MICHAEL AND YOU ALWAYS TALK ABOUT A GLOBAL LIQUIDITY CRISIS PENDING BUT CAN’T WE JUST PRINT OURSELVES OUT OF ILLIQUIDITY?

A: March bank collapses were a result of illiquidity. Simplistically: Money printing creates more debt. As debt increases it gets more expensive, too expensive to pay, higher rate defaults happen. More liquidity crises (private and governments) indeed will happen worldwide. And eventually more inflation.

Q: SEEMS LIKE YOUR FORECAST ON US DOLLAR BEING A RESERVE CURRENCY. ERGO GOING HIGHER IS STILL IN THE CARDS??

A: Ergo, eh? Well, when the Indian Rupee is now going global as 18 countries have agreed to trade in Rupee we need to take note. Also, Saudi Arabia is dealing with China. China dealing with Russia in Yuan’s …etc. NOTE: The world is trying to de-Dollarize the international market amid a global economic slowdown and India and China is turning this into an opportunity. This may not work in the short run….but….stay alert. More under US dollar item.

Q: A few months ago, you mention the de-globalization feature. I can’t find it in Ozbuzz?

A: Agreed. We will do a special feature on deglobalization and de-dollarization.

Q: AS YOU KNOW WE ARE HEAVILY INVESTED IN FLORIDA. GOOD DECISION, I THINK. PRICES ARE STILL RISING AND IT LOOKS LIKE WE ARE NOT PARTICIPATING IN ANY DOWNTURN. YOUR VIEW ABOUT FLORIDA NOW?

A: Well, some markets are still rising in FLA, the majority is not. What we were concerned about was the fact that we as foreigners can’t get insurance (flood, hurricane etc.) or only at great expense. This has become a real big deal for ALL Floridians now. Flood insurance is now mandatory. The incessant floods and storms have bankrupted Florida insurers. Below note these companies that are going bankrupt … just at year end: Insurers in Liquidation AMERICAN CAPITAL ASSURANCE CORPORATION, AVATAR PROPERTY AND CASUALTY INSURANCE COMPANY, FEDNAT INSURANCE COMPANY, FLORIDA SPECIALTY INSURANCE COMPANY, GUARANTEE INSURANCE COMPANY, GULFSTREAM PROPERTY AND CASUALTY INSURANCE COMPANY, PHYSICIANS UNITED PLAN, INC.SOUTHERN FIDELITY INSURANCE COMPANY, ST. JOHNS INSURANCE COMPANY, INC., UNITED PROPERTY AND CASUALTY INSURANCE COMPANY, UNIVERSAL HEALTH CARE INSURANCE COMPANY, INC. UNIVERSAL HEALTH CARE, INC., WESTON PROPERTY & CASUALTY INSURANCE COMPANY, WINDHAVEN INSURANCE COMPANY.

Major Point: Now maybe new premiums are bankrupting YOU! We hear rates are soaring! Buy only with insurance subject clause! (Flood insurance now mandatory.)

Q: THE CANADIAN GOVERNMENT DID THE RIGHT THING BY RAISING RATES TO CUT DOWN INFLATION. WHAT ELSE COULD THEY HAVE DONE? YOU CAN’T BLAME THEM FOR EVERYTHING. Political statement. Inflation will be beaten.

A: If you think my pearls of wisdom are political you are wrong. I have argued against continuous government spending in 5 books and a thousand stories (starting in 1995 in my book “Forget About Location”). Simplistically, Keynesian thinking was, spend in slow times and pay it back in good times. However, our government decided to dramatically increase government spending in good and bad times and then – to boot – crash interest rates to zero. I predicted the only outcome would be higher inflation in all hard assets.

Ok, the government realized it must do the “right thing” and raise rates. But they also RAISED their spending even more! A vicious circle. Inflation will come back with a vengeance.

TOILETS OF THE WORLD

Toilet with a view:

THE NUMBERS, THE NUMBERS

CANADA REAL ESTATE – MUCH BETTER!

The fine Real Estate Magazine REM published a realtor survey which does a snapshot of cross-country activity – reported by local realtors. From Halifax outward there seems to be a tad more optimism, a bit more action, sharply lower new listings. The magazine is a good read and the story gives you stuff to ponder.

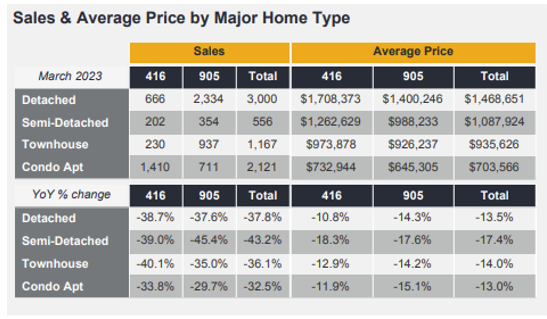

TORONTO

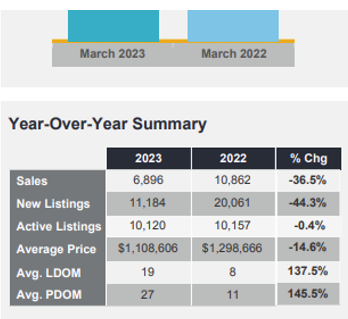

The TREB reported that it thinks competition between buyers is on the rise. 6,896 sales took place – down 36.5 per cent compared to March 2022. On a month-over-month basis, actual and seasonally adjusted sales were up. The MLS® Home Price Index composite benchmark was down by 16.2 per cent. Similarly, the board reports that the average selling price was down by 14.6 per cent year-over-year to $1,108,606. Month over month that is correct. Measured against the high, declines are far larger.

Study the numbers. Official price declines range from 13% to 17% . Toronto Market High of 2022 versus March 2023 shows them to be higher

Again I compare high of 2022 to today. The numbers will continue to get ‘better’ as we compare today’s sharp decline in sales, to the declining numbers of last year!

Major Point: Nationally prices are up about 1% March over February (normal). But areas even suburbs vary – see below in Vancouver.

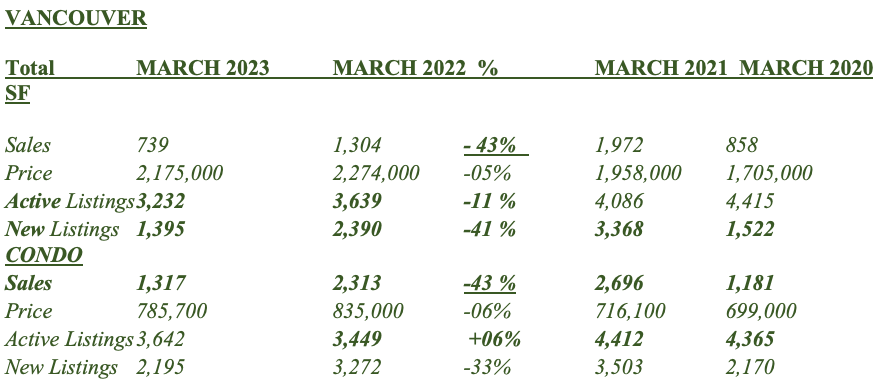

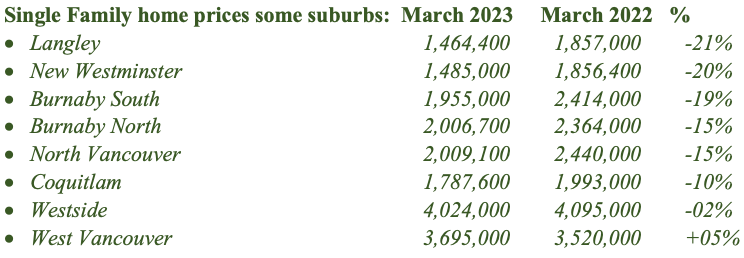

VANCOUVER

Interesting numbers jumble this month. Prices are (somewhat) all over the place, depending on where you are and what you are looking for.

NOTE:

- We separate SF and Condo numbers we do not bundle TH, SF, and condos together and we benchmark nothing.

- We get you to take a look at what the highest price that was achieved in 2022 versus the March 2023 price. Sales and prices separated by condos and single family.

- Then we also give you 4 years of “March” to get an idea how this March stacks up against those last 4 years.

Finally note that from hereon in, all numbers will look better!

Sales started to crash in March/April and kept crashing till now (we are still down over 40% in sales across Canada).

Why will we look better…well, we will be measuring monthly declining sales of 2022 against declined sales 2023 and they will all look much better every month.

Snapshot:

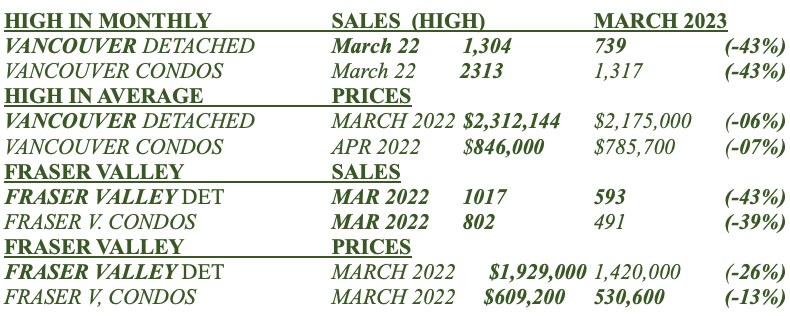

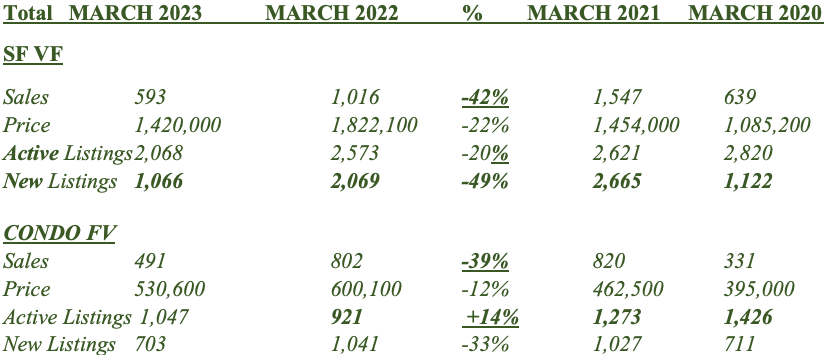

SF: REBGV reported SF sales declined a further 43% over MARCH 2022. The average price high achieved in April of $2,312,000 HAS recovered to $2,175,000 only down 06%.

CONDO: REBGV reports condominium sales are down 43% over MARCH 2022 sales. The condominium average price is down by 7% from April 2022 and 6% over March 2022

Again, For the ‘real market conditions’ we show the 2022 HIGHEST MONTH (first).

Below: Here we are looking at a 4-year MARCH 2022 over MARCH 2023/2022/2020 comparison. Still: Remember to take the 2020 comparisons with a grain of COVID salt!

- Major Point: Note the downturn from the high month(s) in the opening. Active listings – are up 6% in condos but surprisingly down in SF homes.

- New listings are still way down in Vancouver overall.

- Market more active overall…but then it’s spring!

- Note the numbers “all over the place.”

FRASER VALLEY

SF home sales continued their sharp downturn (-42%), but not as badly as the previous month (-60). Prices are still 26% lower than high, 22% lower over March 2022. Active SF listings (+49%!) as well as condominium listings are up a whopping +112%! Condominium sales cracked as well, down 52%.

The numbers tell the story. Things are looking better. Sales way still down but active listings are shrinking. Price declines still sharp – but shrinking. We have started bottom building. Not there yet … but investors … WAKE UP!

MAJOR, MAJOR POINT:

Ozbuzz investors: You faithfully read the Ozbuzz, sold your losers last year, got some ‘market cash’ and some ‘age related cash’ (What is it? Look it up in Ozbuzz 78/80) and now get ready to pounce. This is slowly becoming YOUR market!

You need to:

- Believe in the future of the world’s troubles! We will muddle through.

- We will have higher inflation always eventually … only way to pay the debts. It can never be repaid any other way.

- We will have higher prices … may take a while.

- Investors jump in when everyone else is running away.

- Check your assignment offers in Craigslist, Kijiji

- Make stink bids!

- Surrey. If it was a hot market last February 2022 to spend 1$.9 million on a SF home, it is a scorcher to spend only 1.4 million for the same house!

- MOST Important thing that could be game changers this year? Watch change oil, stocks, and real estate? The war ends. (Putin dies?) Until then stay out of Europe. But there are always opportunities.

WANT TO PARTICIPATE?

Go to www.realestatetalks.com – Some 2,500 members (47,009 posts) talk real estate. Ozzie created this bulletin board in 1998!

If you are in a real estate related industry of any sort (realtor, appraiser, lawyer, home inspector, etc.) list yourself in Ozzie’s free British Columbia real estate directory at www.bcred.ca.

OZZIE’S YOUTUBE CHANNEL

You can watch all videos and podcasts on my YouTube channel at https://www.youtube.com/jurockvideo. It is a great way to check on what I said 10 years ago.

Moneytalks Podcast

Ozzie, Michael Campbell, Michael Levy and Victor Adair and guests are now on podcasts every week: https://omny.fm/shows/money-talks-with-michael-campbell (See Victor Adair’s Trading Desk notes! https://victoradair.ca/)

OZBUZZ.CA

Why subscribe if I can just go to the website at Ozbuzz.ca? Hot properties and the latest podcasts are DISTRIBUTED TO SUBSCRIBERS FIRST– posted 2 weeks later on website.

HAVE A QUESTION OR COMMENT?

You can reach me at info@ozbuzz.ca with all of your questions, comments and concerns regarding the Oz Buzz publication.

| Subscribe to Oz Buzz: |

(You’ll get Oz Buzz 2 weeks before it’s posted online)

Leave A Comment