“Why do men like intelligent women? Because opposites attract.”

July 14, 2023

AGENDA

- BOC SOCKS IT TO US

- LIES, DAMNED LIES AND STATISTICS

- AIRBNB COLLAPSING

- INTEREST RATES AND THEN INTEREST RATES

- THE MARKET IS HOT. THE MARKET IS NOT HOT

- INFLATION UP OR DOWN?

- OZBUZZERS ARE ALSO CONFUSED

- THE NUMBERS ARE BETTER IN JUNE OVER 2022 BUT NOT 2021

- QUESTIONS, QUESTIONS

- YESTERDAYS’ DREAMS TODAY’S REALITY

WE WANT CLARITY BUT WE ARE CONFUSED

Lots of comments on the ‘world economy and inflation pieces.’ Sad to say, we Ozbuzzers are not different than the rest of the forecasting brigades. Comments pound in … both for and against inflation and for or against recession and ‘8 outliers’ – total collapse, the big reset, we own nothing, digital money, ESG is for losers and needed for making investment decisions … etc., etc., etc.

WE WERE WAITING FOR BANK OF CANADA

Yes, BOC increased interest rates by 25 basis points (as predicted). That is now the highest level since April 2001. In the face of ‘falling’ inflation.

BOC’s rate (benchmark) now has hit 5%. Man, that’s up 4.75% since March 2022. 10 increases in the last 16 months.

As I maintained and still maintain – it is NOT the rate itself (we can get used to it) but the speed of the rate increase that hits us over the head with uncertainty, doubt, and outright fear!

They fooled us by pausing in March and April, now it is back on the ‘raising train’ (twice in a row). Why? 60,000 new jobs this month, ‘sticky’ inflation?

Yes! But these raises … together with BOE (up .75% in a month) and all other Central Banks … I am fearful that CBs are fearful!

Q: I KNOW, NO ONE CAN TELL INTEREST RATES. BUT YOUR BEST TAKE?

A: No one knows the eventual outcome. The BoC was expected to raise rates by 25 bps on July 12 and it did. The US Fed and the ECB are expected to raise rates by 50 bps before December, while the BoE is expected to raise rates by another 100 bps (?!) before year-end. The point? Inflation is much more of a problem then what they actually publish.

LIES, DAMNED LIES AND STATISTICS (DISRAELI)

We told you last year that as we (WILL) compare ourselves in 2023 to the same month in 2022, we will look great! In fact, for several months last year after May sales were down 40% to 50% every month over 2021 – so – said we – 2023 will be looking good…

And we are! Yes – somewhat.

But note:

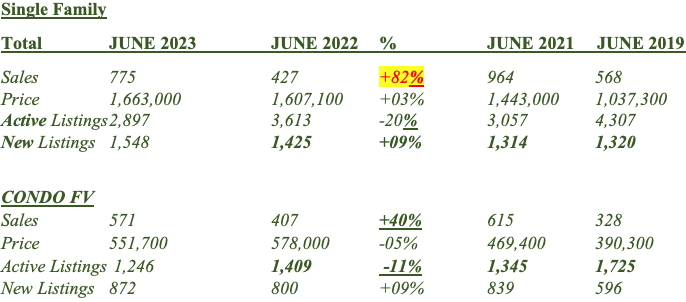

Yes, Fraser Valley SF homes are up 82% with only 775 sales … why? Because last year in June we performed at an anemic 427 sales rate.

In June 2021 we had 964!

So, Beer? Yes! Champagne? Not yet!

SAME FOR PRICES. NOTE:

Surrey SF 2022 Feb $1.9 mill, Surrey SF 2022 December $1.3 million, Surrey in June 2023 $1.55 mill.

Better price yes, but not back to previous high. FOR DETAILS LOOK AT The Numbers below.

QUESTIONS, QUESTIONS

Q: I am an ardent reader of your weekly newsletter since 2005. I seem to note some confusion in you. Inflation, runaway inflation, stay in cash? Do you still like real estate?

A: That question is most surprising to me. I have NEVER (NEVER, EVER) wavered in my stance on owning real estate. Always a buyer, holder, and collector of real estate. Homeowner – buy, buy. Investor? As long as you understand the 4 macro and 4 local influences that should govern your PERSONAL decision. (Revisit Ozbuzz 38 – 42 … each issue features a snapshot of my philosophy).

But just because I believe in real estate ownership (primarily leverage), there are considerations. Inflation? Yes. Timing? Yes. Trend? No. Cycles? No. Right now (and that may be confusing to you) I prefer to sit on sidelines (as an investor) and wait for clarity. Have my powder dry and get paid for it (5.6%). If I miss the absolute bottom, that’s fine … but I want to be sure that hard asset inflation remains the outcome – and not another big dip.

We said elsewhere that I look for a recession followed by hard asset inflation. Question remains to be timing. Now whether or if, but when!

Some of you missed:

- Motivation card – Well, we did the whole 50 card set twice (I put one of my favorite one in today – Dream Big) http://commitperformmeasure.com/

- Songs of the week – Ok, here goes: ‘Oh Lover’ (Roeksopp) https://www.youtube.com/watch?v=C0vukFNMb7I

- Bingeworthy – The new STAR TREK – STRANGE NEW WORLDS – ok. Not the same – but for the nostalgic ones – it grows on you. 19 episodes.

- Toilets of the world – Can’t find any new ones – how many do you think there are?

Q: I liked checking out shadowstats.com, your debt graphs. Eyebrow raisers!

A: Yes, indeed, only none of the graphs in the last Ozbuzz were mine. (They come from indicated websites).

Q: Runaway inflation – no way. I thought. But then why are they raising rates everywhere after we were told, raising was over? Yes, they seem scared. Keep writing.

A: Runaway inflation? I called that an outlier… More interesting… Literally 4 days after I told you about the various interest rates increases in the world (including England on May 8) … England raised its interest rate again and for a half of one percent. So, .75% in just one month!

Q: Inflation is going down everywhere. Are we in for stagflation, recession?

A: Stagflation, deflation, recession – all in the cards. All a matter of when not how. Hard assets will rise. Period. Recession very likely fourth quarter or next year. But the eventual outcome (as far as we investors are concerned) are higher real estate prices. Just when is the sticky question.

Q: I wish you had a US only version. US mortgages are mostly 30 years. So not comparable. But I can’t get a business loan!

A: Very good question. That is not even the only difference. Generally, US SF homes are a LOT cheaper than major cities in Canada. Also, most households have locked in their mortgages at under 4% for decades. Then there are different government programs and points to brokers … all are different. The biggest difference is found in commercial lending. The US has 4000 banks (most with one branch. Canada has 5 banks with 4000 branches, or so).

In the US when the FED sharply raises rates, it mainly hurts smaller regional banks (Silicon Valley bank and 50 others). As well as all commercial real estate and small businesses that rely on bank loans. That is not going to change. It may get worse if the FED follows through in is promise (threat) of 2 more increases in 2023.

Q: Where do you get your stock information? Michael Campbell?

A: Yes, but not only. Note, I’m not a stock market guy. I’m only interested in what events take place in stocks, that may impact real estate action/values. I do read Victor Adair’s Trading notes religiously. Victor Adair’s Trading Desk notes! https://victoradair.ca/

For instance, Victor writes: “I get most of the ‘Magnificent Seven’ (AAPL, MSFT, GOOG, AMZN, NDVA, TSLA, META) have a combined market cap of ~$11 trillion and have risen ~60% YTD. The remaining 493 other S&P 500 stocks have a combined market cap of ~$25.7 trillion and are up ~5% YTD.” What do I get from that? If you are not in the 7 stocks, you are only up 5%. No impact on real estate.

Q: Why did you drop the “Major Point”? I am used to go from point to point. Now it is ‘note’.

A: If that is your only problem, my world is ok.

Q: Everyone said that mortgages that are coming due for renewal are going to be a problem, but it has not had an impact. What impact?

A: Roughly 1.1 million Canadians will have their mortgages come up for renewal this year. (BOC). However, most fixed-rate mortgages will face renewal in 2024-26.

Increases in monthly payments:

- Fixed rate payment increases expected to be 20% to 25%.

- All adjustable-rate borrowers (those whose payments vary as interest rates change) have already experienced payment increases, with some seeing their payments surge by more than 50%.

- Google mortgage default, there are tons of stats.

Q: A nod to Elon Musk: The laptop crowd lives in la-la-land. Oh man, you gotta love it!

A: It is a great interview. Go see it on YouTube. I mean working at home is “really a moral issue”?! Hmm, the guy does have brains. As an old manager, I also would want my gals and guys to be in the office. (I know, I know – just saying.)

Q: Why can banks charge unconscionable penalties?

A: Question is, why don’t buyers EVER read their mortgage documents? However, our fearless government agrees with you. On July 4 they released a ‘guideline report”, to standardize how Canada’s federally regulated lenders offer mortgage relief to consumers with a new approach. This could save some mortgage holders on costly fees and penalties that come with refinancing, paying lump sums, or otherwise altering the terms of their loans. Read it here: https://globalnews.ca/news/9811866/mortgage-relief-guidelines-canada-interest-rate/

The catch? Don’t hold your breath. It is only a recommendation to the banks, not an order or a law…

Q: I hear there are new rules forbidding multiple offers?

A: No, not forbid them, but new regulations for realtors and owners on how to report them. New guidelines for multiple offers include a new form that has to list all offering brokerages that made an offer, signed by the owner and the listing broker. That form will state that an offer was made, the date and which Realtor. This form is not helpful for buyers since it is delivered only AFTER the owner accepts an offer. (Buyers still don’t know the competing bids – price-conditions.). However, a successful bidder can now see who else is in the game and under the “cooling-off period” legislation he can still walk away.

Q: We bought an Airbnb in 2021. We did great until about mid 2022. Our rental income is now down to less than half of what it was. Is there a general Airbnb Collapse?

A: You don’t say where you have your building. I’ve never run a BnB, but as an old property manager – when business got down, I got going – taking business from competitors. If your business is down because of more competition – get to be a better owner. If your business is down because of fewer travellers – get in the listings of all travel agencies. If you have a few bad reviews – work HARD to answer them right away – friendly but firmly. Travellers read reviews. If you have unruly people expecting hotel service with Airbnb – make sure you spell your rules out online. Whichever organization you use, Hotel, bookings.com, etc.- read the rules.

Here is an article reporting a downturn in the US.

Q: Your recommendation to change your US dollars back when the Canadian hit 72 cents was right on. I wish I had.

A: By ‘changing back home’ you mean exchanging your US dollars you hold now into Canadian dollars. Yes, the Canadian Dollar hit a 9-month high above 76.6 cents on July 14. Those of you that exchanged in the 72/73 cent range are smiling. The US dollar took it on the chin this week but in our view will still remain the reserve currency of the world. The Canadian dances up and down with oil and US interest increases. Unless we match US increases, we drop and if we are in front of the US (as now) we rise. As always, it’s not important to be right, but to understand the timing of a thing!

Q: On your story on Florida crazy insurance rates. It is unbelievable how insurance companies get away with these fees. They refuse to pay Earthquake damages to homeowners.

A: Well, I admonish them too: But, read your insurance docs. You don’t get what you don’t pay for. There is a lesson here for Vancouverites and all costal cities. Right now, earthquake riders are not that expensive (until there is a quake). Get earthquake insurance. These Californians didn’t: https://www.cnn.com/2023/07/02/us/rio-dell-california-earthquakes/index.html

Q: I wish you would do a deep dive into why it is not alright to have government pay its poorer citizens by just printing the money needed. Here in the US, we created a lot of programs funded by our president with the result of lowest unemployment, highest employment, and wage growth ever.

A: Also, the highest cost of goods and services EVER. Printing money means, creating debt. Creating debt means paying interest. Simplistically, with every 1% increase in interest rate on the $32 trillion US federal debt results in $320 billion worth of additional annual interest expense. That’s equivalent to the government hiring 2 million people at $160,000 per worker per year. (Alden). Just extra interest. So far in the US the interest rate has been raised by about 4% – you work it out for Canada.

Major Point: We can NEVER pay it back. They WILL pay it back ONLY with higher inflation. To protect yourself … watch your world carefully and when sure – get and stay in hard assets.

Q: Major malls are closing in Chicago, Portland, LA. Now a major San Francisco mall is closing (Westfield) and Westfield movie theatres. Why do they let it happen?

A: Who is ‘they’? These cities represent the changing woke world (Westfield just follows Nordstrom, Old Navy, and the Gap.) Woke cities will end up with what they want. No police, no bad guys in jail, no bail, no stores open to rob. Also, the 1,921-room Hilton San Francisco and the 1,024-room Parc 55 San Francisco gave back the hotels to their mortgage company. They gave up! We recommended at length in 2021/2022 to get out of woke cities and go to Texas, Florida, and Arizona.

Q: So many questions on rates, the why, the how and the wherefor and what now?

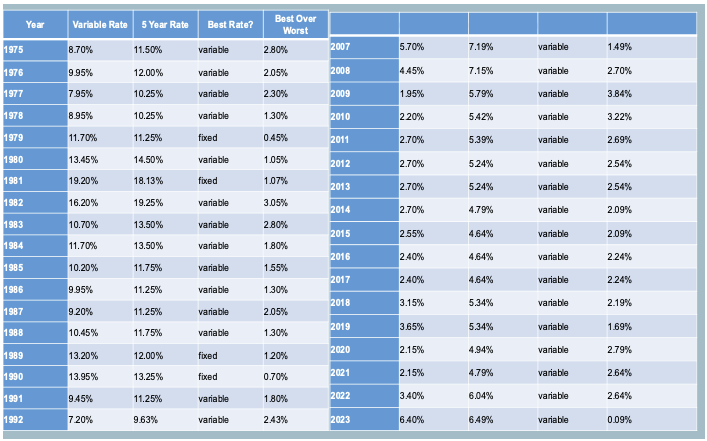

A: Please note that the current Canadian 5-year rates in the 5 – 7% rang are (I know, I know) just fine – historically speaking. Look at the chart below. In almost 50 years the 5-year term rate has been below 5% only in 2014, 2015, 2016, 2017 and 2020. 5 times. And most of the time it was far higher! What is new is, that people absolutely believed in short term variable rates and HELOCs. In my previous newsletter Fact by Fax, I talked continuously against the HELOCs, that banks and their brokers were pushing. A sure-fire way to over-borrow.

Q: Our residential market is soaring, why is commercial lagging?

A: It isn’t just Musk’s Lalaland crowd that is NOT going to the office. We just simply need less space. The large legal libraries in a law office are now stored in the cloud. As are trillions of other documents. So, there is a general declining demand for office space. Result? Office real estate asset valuation is falling. Owners that went short on their mortgage terms face renewals at astounding increases in cost at the same time as tenants need less space. Banks look at the appraisals that they have on file on their loans with suspicion. Other commercial assets (multi family) have faced tenants that can’t/won’t pay, went short on interest rates, costs are rising … so commercial is not only lagging but falling in value. That can all change on a button if the Central Banks pivot. They will. Question is, when?

COMMENT: Gals and guys you have too much on your mind on LGBQT, Disney, Target, Netflix … a hundred others.

Too much for me….

My Ozbuzz ROTLM is the revenge of the little man not a mass boycott. Although…ha-ha…

Ozbuzz’s ROTLM will take a break here.

I will however – in my ‘little man capacity’ keep on exacting my revenge. (Self check out at shoppers, no bagging at Safeway and other wonderful ditties).

Q: MICHAEL CAMPBELL HAD A GUEST WHO SAID, “YOU WILL OWN NOTHING”?

A: In the line of the ‘great reset’ piece we did a couple of months ago, this is a ‘must listen to’ podcast from July 8, 2023: https://mikesmoneytalks.ca/july-8th-episode/

Comment: Lots of questions on ESG stocks. Here is a fine outline by Fasken. The End of the ‘Alphabet Soup’ for ESG Disclosure Requirements and how will Canada position itself?

Not so good news:

- The quarterly MNP Consumer Debt Index out July 12 showed that Canadians who report being insolvent have reached a record high. More than half of the 2,000 Canadians reported that they were $200 or less away from not being able to meet their financial obligations.

- Statistics Canada says that a downturn in building permits accelerated in May (BC). Building permits for the month totaled $1.5 billion, down from $2.3 billion a year ago. Year-to-date numbers are even less encouraging, with a 43 per cent decline in Chilliwack contributing to a 20 per cent decline province-wide in the first five months of the year to $7.5 billion in building permits. This was part of a broad-based and accelerating decline versus the first quarter. Alta is down also, except for Calgary which is substantially higher!

- There is no clarity – confusion reigns worldwide….

THE NUMBERS, THE NUMBERS

BRITISH COLUMBIA

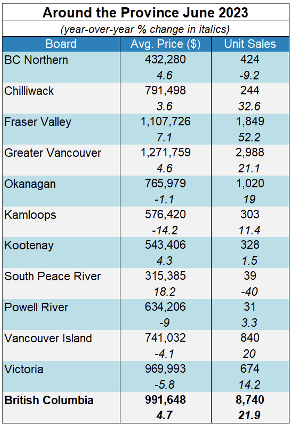

The fine British Columbia Real Estate Association reports that active listings in the province were above 30,000 units for the first time since September 2022 (still down 1.2 per cent over 2022). Year-to-date BC residential unit sales were down 21.1 per cent to 40,381 units, while the average MLS® residential price was down 6.4 per cent to $976,885.

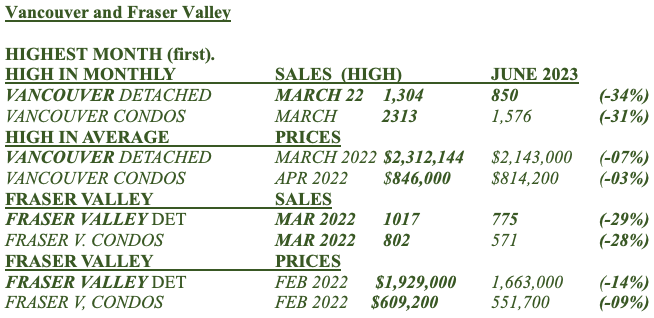

VANCOUVER AND FRASER VALLEY

We told you last year that, as we compare ourselves in 2023 to the same months in 2022, we will look great! The market collapsed last year – now it has recovered? Yes – somewhat.

Note: Fraser Valley SF homes are up 82% with 775 sales…why?

Because last year in June we performed at an anaemic 427 sales rate. In June 2021 we had 964 sales…

So, Beer? Yes! Champagne? Not yet!

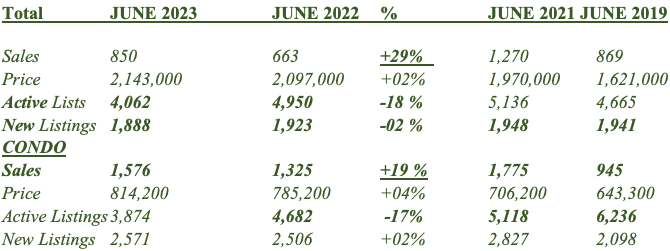

Vancouver and Fraser Valley

VANCOUVER

May 2023 showed 1,047 SF sales and that was 31 % higher than the 797 sales of May 2022

June 2023 showed 850 SF sales and that was 29% higher than the 663 sales in May 2022

However, sales in June 2023 are down from May 2023 by 197 SF home sales or -20%. Usual seasonal change (-10%)

Also:

May 2023 showed 1,732 Condo sales and that was 8% higher than the 1,604 sales of May 2022.

June 2023 showed 1,576 Condo sales and that was 19% higher than the 1,325 sales of May 2022.

However, sales in June 2023 are down from May 2023 by 156 Condo sales or -9%.

(Seasonal change as we slow down into the summer.)

NOTE: Sales of SF homes are still lower than 2021 or 2019. Sales of condos lower than 2021.

AGAIN: We left out JUNE 2020 because of covid. So, we put 2019 instead!

Below we are looking at a 4-year JUNE 2023 over JUNE 2022/2021/2019 comparison.

- Major Point: SF Sales are up 29% over 2022. Still sharply lower than 2021.

Active listings – are down 17% in condos; down 18% in SF homes. - New listings are down 2% in SF homes, UP 2% in condos.

- Markets are still more active overall. How much the increase of rates in 7% will play a role…remains to be seen. We expect the next .25% increase to flatten any increases in volume or prices. (July 12)

The Vancouver and Fraser Valley Real Estate Boards have the BEST current statistics.

Get your professional realtor give you the numbers for the sub-area that YOU are interested in.

FRASER VALLEY

- Major Point: SF Sales are up a whopping 82% over 2022. Still 18% lower than 2021.

- New listings – are up 9% in condos; surprisingly and also up 9% in SF homes. Markets in the valley are more active overall…

In March/April/May we said: We have started bottom building. Investors …WAKE UP! You woke up … We are still not back to 2021 volumes but nicely recovering from the doldrums of 2022. Except for the continued interest rate increases… Investors, this is slowly becoming YOUR market!

MAJOR, MAJOR POINT:

The summer will be slower, new rates will bite. Look for good deals only. Assignment offers are mounting. Costs of construction is soaring. Rumours of some developers not proceeding – giving deposits back.

Commit Perform Measure

Yesterday’s dreams form today’s realities = Think about it!

WANT TO PARTICIPATE?

Go to www.realestatetalks.com – Some 2,500 members (47,009 posts) talk real estate. Ozzie created this bulletin board in 1998!

If you are in a real estate related industry of any sort (realtor, appraiser, lawyer, home inspector, etc.) list yourself in Ozzie’s free British Columbia real estate directory at www.bcred.ca.

OZZIE’S YOUTUBE CHANNEL

You can watch all videos and podcasts on my YouTube channel at https://www.youtube.com/jurockvideo. It is a great way to check on what I said 10 years ago.

Moneytalks Podcast

Ozzie, Michael Campbell, Michael Levy and Victor Adair and guests are now on podcasts every week: https://omny.fm/shows/money-talks-with-michael-campbell (See Victor Adair’s Trading Desk notes! https://victoradair.ca/)

OZBUZZ.CA

Why subscribe if I can just go to the website at Ozbuzz.ca? Hot properties and the latest podcasts are DISTRIBUTED TO SUBSCRIBERS FIRST– posted 2 weeks later on website.

HAVE A QUESTION OR COMMENT?

You can reach me at info@ozbuzz.ca with all of your questions, comments and concerns regarding the Oz Buzz publication.

Please note that any response to any email or any invitation to any meeting is accepted on the understanding that “Jurock Real Estate Insider (JREI)”, “OzBuzz (OB)”, “JCIR (JC)” as the case may be, are not responsible for any result or results of any action or actions taken in reliance upon any information contained in this posting or meeting, nor for any errors contained therein or presented thereat or omissions in relation thereto. It is further understood that the said OB or JREI, or JCIR as the case may be, do not, pursuant to this posting, purport to render legal, accounting, tax, financial, planning, or other professional advice. The said OB and JREI and JCIR may or may not own properties discussed at meetings or receive or not receive referral fees at any meeting you may attend as a result of this posting or invitation. The said OB and JREI and JCIR, as the case may be, hereby disclaim all and any, liability to any person, whether a purchaser of any offering, a reader of any offering, or, otherwise, arising in respect of this postings and of the consequences of anything done or purported to be done by any such person in reliance, whether whole or partial, upon the whole or any part of the contents of these postings. If you respond to any posting OB or JREI and JCIR or attend any meeting from and by said companies, we fully expect that you get independent legal/tax/investment/mortgage advice as the case may be.

| Subscribe to Oz Buzz: |

(You’ll get Oz Buzz 2 weeks before it’s posted online)

Leave A Comment