November 20, 2023

Q: What does Living Life Large mean?

The four pillars of happiness are loving and engaged relationships, a sense of purpose, an attitude of optimism, and a connection to spirituality. All four pillars support a happy life. If you are unhappy, the first step is to identify which area you’re lacking in.

Latest OZZBUZZ Ozcast VIDEO and OZBUZZ Podcast AUDIO: Watch videos:

We predicted it last month: Killed in BC! Short term rentals! BC Government declares ‘Death to an industry’.

Real Estate Talks: Ozzie says buy or sell?

Real Estate Talks: Ozzie in Late October: New law: 6 properties on a residential lot?

Or…Listen to all videos on Podcast: (on Apple cast, Amazon video, Spotify and Ozcast): https://ozbuzz.ca/category/podcasts/

Listen to Ozbuzz in your car

Topics: On Airbnb, On SRT, On upsizing retirees, on UHT, on interest rates, on markets ahead.

On November markets, On Edmonton, On interest rates…

AGENDA

- NEW AIRBNB TAXES (NOV 21)

- THE DEFINITIVE OUTLOOK FOR INTEREST RATES. WEIMAR AHEAD?

- LAST MONTH RUMOUR – THIS MONTH LAW -STR

- AS PREDICTED MARKETS ARE COOLING BUT FOR HOW LONG

- THE NUMBERS, THE NUMBERS – TORONTO-VANCOUVER

- INFLATION/RECESSION?

- OUTLOOK

- WHAT TO DO IN DECEMBER

- QUESTIONS, QUESTIONS ARE BACK IN PRINT

- SOLAR PANELS? YES, OR NO?

- EVs? YES OR NO.

- CLOSE ON YOUR PRE-SALE. HERE IS WHY.

COMMENTS

Our short ‘Q&A on video’ test showed between 500 and 1000 views per show. But we also received a very large number of notes liking the written version a lot better.

Q: Comment: A cute letter spelled it out thusly (yes, thusly):

G. M. writes: “Some time around the 6th of every month my wife (of 41 years) and I are abuzz looking for Ozbuzz. By the 10th we accuse each other. I’m sure you deleted it by accident, check it, my wife says. And so on. Now we have to learn YouTube. We’ll just have to read the Ozbuzz twice to get the same ‘buzz’ without the great questions.”

A: Love this. 41 years married? You guys and we guys (we have you beat a few years) are a rare breed. We stay together! The secret? We never go to bed mad (we stay up and fight)… My best friend says he is also married 45 years … but it is his 3rd wife! Anyhow I hear you, We put the Q&A back for now and change the video to “one topic shows”. Go view at www.youtube.com/jurockvideo or listen at Oz cast (on Ozbuzz.ca).

THE WORLD, ECONOMY, INFLATION ETC.

The constant questions on interest rates, wither the market show the great concern ANY THINKING PERSON (and Ozbuzzers are thinkers!) has. It is indeed a strange situation we find ourselves in. Let’s look at interest costs to government and individuals, inflation/deflation and try and make sense of what confronts us.

INTEREST RATE COST TO GOVERNMENT

CANADA: Our government (actually all governments worldwide) have been spending money like the proverbial drunken sailors – using the excuse of Covid and never having to content with a rising interest rate environment. Now with rising debt payments and companies making less money (spell lower tax income) there will be the double whammy: More and more debt costs and taxpayers fed up with always higher and newer taxes.

US: As I said on my YouTube video a couple of weeks ago … go to https://www.usdebtclock.org/ and weep. Debt and debt payments are massive. US interest debt payments stand now at a whopping $1.027 trillion! Just 2 years ago, annual interest expense on US debt was at $450 billion.

Major Point 1: That’s a 128% increase in just interest payments WITHOUT a recession yet.

Major Point 2: Since 2020, total US debt is up ~$10 trillion and set to hit $35 trillion in 2024. The debt payment is now approaching the total cost of the total US military!

That is Weimar Republic stuff! It was 1920-1923 when war reparation and interest payments in the billions that Germany had to make to the Allies that sank the German Gold and Paper marks. Only by printing larger and larger quantities of money (my grandmother couldn’t buy an egg because it cost 2 million … and she only had 1.6 million!) could they make the payments until it all collapsed. (BTW, if you had hard assets like real estate, you were a Weimar survivor.)

Major Point 3: Are we there now? No, but we have eyebrow raising similarities – worldwide.

RECESSION OR NOT?

Q: You have forecast a recession all year. It didn’t happen. Are you still forecasting one?

A: Not sure I forecast a recession ‘all year’, but certainly since the summer. Yes, in our opinion, we will have a recession in the 1st quarter (with the usual ‘if’ provisos). We currently have massive layoffs in a lot of major corporations. The auto industry is tanking (don’t buy a car till late December or next year). I mean TANKING! EVs sales have collapsed. I mean COLLAPSED! Banks are using tighter and tighter borrowing restrictions. I mean TIGHTER!

INTEREST RATES IN A RECESSION

If we get into an “admitted” recession (we are really already technically in it – aka Rosenberg) we will see a ‘stoppage of increases’ of rates. There also will be a pressure on government and the BOC to lower rates just to deal with mortgage renewal issues ($184 billion in 2024 and $350 billion in 2025). So, depending on the speed with which we turn down (and we are turning down) we could see a reduction of .25 percent as early as April perhaps another .25% by midyear.

Esteemed Dr. Thorne on a recent Michael Campbell podcast expanded on his view that recession and lower rates are coming early next year. Benjamin Tal sees rates lower between April and July.

Our view remains that there will be no return to the low, low rates of yesteryear! That would affect short term and variable rates. The stress test will stay (now around 9%).

Long term rates, as we have discussed many times are directly related to the bond market. That’s why US 30-year mortgage rates hit 8% (briefly), when 10-year US treasuries hit 5%.

MAJOR, MAJOR INTEREST RATE POINT: THE BIG QUESTION

Why are there so many differing opinions? The fact that 10-year rates reversed back down to 4.5% has created a new problem. With the U.S. national debt surpassing $33 trillion and interest payments of over $1 trillion – ditto huge debt payments for Canada – and the US credit rating in question (Moody downgraded future outlook) foreigners no longer have an insatiable appetite for U.S. government debt. WSJ: ‘That’s bad news for Washington’. The U.S. Treasury market is in the midst of major supply and demand changes. The Federal Reserve is shedding its portfolio at a rate of about $60 billion a month. Overseas buyers who were once important sources of demand—China and Japan in particular—have become less reliable lately. Question? Temporary? What are they expecting to happen?

Why talk US … we are in Canada? Agreed, but as the US flies, so do we in Canada, with over 80% of US states dealing with a Canadian province – buying or selling – we are married at the hip. Like it or not.

Ok, what will the rates be?

- I expect inflation in hard assets – massive measurable inflation – to return in 2 – 5 years. All other non hard assets are already inflating at astounding HIGHER rates (food, rent, restaurant meals, all double digits, etc…, etc…, etc.).

- Official reported rates are not real (watch shadowstats.com) and/or Prof. Steve Hanke

- US election year usually leaves the Federal Reserve on sidelines. They do not wish to be seen having monetary policy that could influence elections. Generally, rates were low and steady in past elections.

- With mortgage renewals at almost $500 billion in Canada in next 2 years, the government will make every effort to keep rates the same or down … or allow 50-year amortizations or other initiatives (force banks).

Q: Why are so many mortgages coming due in 2025? Who says so? I would think all renewals have been done.

A: Google the RBC October report. It states that approx. $184 billion in 2024 and $350 billion (or so) in 2025 are due. Why? People in 2020 were worried about Covid, the world was uncertain so they took (massively) a 5-year rate ($350 billion). By 2021, rates came down further, banks pushed Home Equity loans and many buyers went for 3 years.

Final Major Point: In this environment the MOST IMPORTANT THING TO DO is hiring quality PROFESSIONALS. Not all mortgage brokers or realtors are the same. For a professional recommendation send me a note.

Q: With pre-sale markets collapsing, should I walk away from my $72,000 deposit?

A: What pre-sales are collapsing? In any market there maybe pressure on some developers. But in this market MOST presales are closing. Likely bought 2-5 years ago, they are still in profit and are still a good investment with rents soaring and new construction STALLING.

Also, a developer has the right to sue you for more than the deposit. He can sue for specific performance or damages or both! Including the legal costs he incurs to sue you. Get immediate professional advice from your lawyer/accountant/realtor.

That goes for all mortgage troubles: You expect a problem? DEAL WITH IT NOW! See your lender.

Q: Your view on Solar panels is ridiculous. It is the future.

A: Yes, we have been sold a solar future. But think twice. High upfront cost/requires sunny weather/does not work at night/manufacturing of solar panels can harm the environment/low energy conversion rate/panels are fixed at their installed location. You need batteries for backup. Dozens of solar companies have gone broke. If you are a good citizen (I salute you), it will be more costly than you think, create problems you never had before. Google “solar problems” and cry.

Q: Your forecast that the Canadian dollar is tied to oil does not always work out. Particularly lately.

A: Oh really? My forecast was wrong? I mean, how could I possibly have an opinion that did not work out. Are the stars misaligned? My gurus sick or? I don’t forecast, I opine! Actually our dollar danced exactly with oil as it went up and then down…we followed suit. The big surprise is that oil is down with all the wars and uncertainty and the dramatic world we live in. Does it signal slowing global growth ahead?

Q: US dollar up?

A: I like a more specific question please. Up against what? I maintain that US dollar has been and will be the reserve currency for the world … until it isn’t.

Q: I remember you forecasting in 2016 that Donald Trump would win the election. What do you think in 2024. Biden or Trump?

A: In my view neither will run or be elected. A third candidate will emerge and the tired electorate will FLOCK there.

Q: I resent your attitude on Tesla EV. EVs are the future.

A: Why resent? Just disagreeing is enough. Also, I did not make any comments on Tesla cars. I did comments on video as to why I will not buy any EV yet. They are too expensive to buy, too expensive to make (after government subsidies run out), and they are unreliable after 2 years. You can’t get power when you want, where you want. It will be more expensive than gas as our demand for electricity will surge beyond comprehension. Which brings me to…

WHY YOU DO NOT WANT TO BE THE FIRST?

Look all our innovation is great – eventually. But before I adopt it, I remember the pioneers in the American Wild West. They explored, they traveled; they had hardships. They also got killed by the natives. Should they not have explored? Of course they should have! Should I be part of the new pioneers? No I rather become a settler, after the treaties have been signed and peace pipes been smoked…

Today EVs, Solar power, wind (and water) power (closed down everywhere – as soon as subsidies run out) and yes …’AI’ all are in “pioneer” territory. AI? You have not seen anything yet. Is it coming. Of course … but you will have problems you never thought about … as a company owner or an individual user. A new technology faces privacy and hacking issues, software vulnerabilities, interoperability issues and legal liability. Often new AI installations making erroneous assumptions about AI capabilities.

NEW AIRBNB TAXES!!!

(On November 21 – to be announced)

Chrystia Freeland will announce tax changes designed to curb the use of Airbnb Inc. and other short-term rental services.

The government will prohibit property owners from deducting expenses on short-term rentals in areas where those services are already limited by other levels of government, the news outlets said.

The Canada wide tax change, which would come into effect Jan. 1, is meant to crack down on property owners who flout local regulations, according to the Star and La Presse.

“I contend that for a nation to try to tax itself into prosperity is like a man standing in a bucket and trying to lift himself up by the handle.” ―Winston S. Churchill

GOVERNMENTS ARE A FARCE

CMHC will be granted C$15 billion ($10.9 billion) to offer loans to real estate developers at advantageous rates for the construction of rental housing as part of a new housing package, says Finance Minister.

Good you say?

Yes, Michael Campbell and I also recommended on air that government do away with GST on rental construction. They did. We saluted the Feds. Then Vancouver brought in new and expanded old taxes wiping out almost 50% of the GST savings for developers. Huh?! Huh?! The Feds now will reassess its commitment to give the above loans…

Left hand not knowing the right hand (of governments?). Listen to Michael Campbell podcast at https://mikesmoneytalks.ca/category/mikes-content/complete-show/

Q: You used to do more on crypto. What are your views now?

A: Same as always … until the pioneers have all been killed and the settlers signed treaties, I am out. Who will be the settlers? Governments. Look below.

CRYPTO – INTERESTING VIEW

Stablecoins and central bank digital currencies (CBDCs), not crypto, will be part of the financial ecosystem in the future, the managing director of Singapore’s central bank said during his keynote at the Singapore Fintech Festival.

“There are four contenders for digital money,” Ravi Menon said, naming them as privately issued cryptocurrencies, CBDCs, tokenized bank liabilities, and well-regulated stablecoins.

But in Menon’s opinion, cryptocurrencies have failed the test of digital money because “they have performed poorly as a medium of exchange or store of value, their prices are subject to sharp speculative swings, and many investors in cryptocurrencies have suffered significant losses.”

Major Point: Well said!

Q: Your take on Airbnb?

A: We told you in October that “Mr. Eby will bring in new rules on short term rentals province wide”. He did and made a law that overruled all municipalities over 5,000. (Kyle Green (STR owner) and I discuss it at length – see video).

Q: You added Toronto to your numbers. Why not Calgary and Edmonton?

A: Yes, we have 42 new subscribers from Toronto. Alberta will be added.

Q: Your numbers are different than the one from other sources.

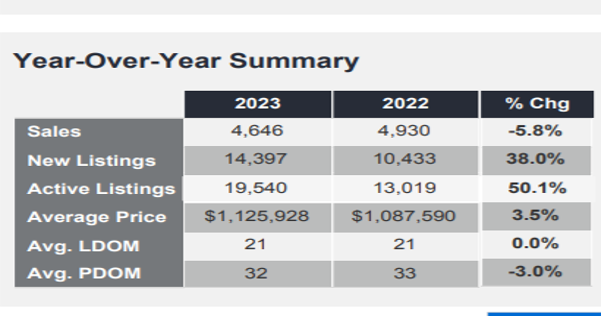

A: Yes, numbers can be confusing. We have written about it several times. When the press quotes an average price (from the various boards) – that price represents the average residential price for all real estate sales – new/used/SF/Condos etc. For Vancouver it covers the area from Mission to Lions Bay(?!). That average price is now $1,196,500. Same for Toronto (see average price below).

So, to make it a bit more understandable, we break the numbers down between SF and Condos (for 30 years). We get a snapshot of what really happened in each sector and we tell our investors to look at area specific suburbs at each board. Arguments can be made for median prices or benchmark prices. We like the average and measure that average for five years each month. It helps you to get an idea what the numbers mean from a general market perspective.

CANADA NUMBERS

Toronto

- Sales in 2022 were already anemic and are now further down by 6% Imagine in October 2021 there were 9,743 sales!

- New listings are up 38%

- Active listings are up 50%

- Prices even with last October but down 30ish percent over March 2022 ($1,980,000)

Toronto numbers

Toronto Real Estate board (TREB has great stats)

Major Point: Lots of videos by realtors on Toronto real estate. All negative.

As an old branch manager I went through many downturns. My favorite 3 words to my salespeople? SO WHAT? NEXT!

Maybe sales are down and go down further, maybe even 30% further. So what, get your property into the 70% that sell!

Dear reader: Pick your realtor carefully. And get a quality mortgage broker.

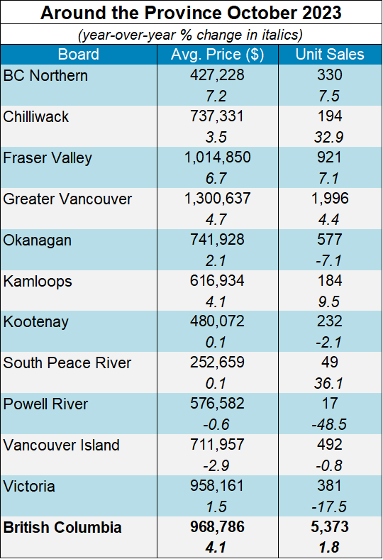

BRITISH COLUMBIA

The British Columbia Real Estate Association – bcrea.com (Best stats, easily presented) reports 5,373 sales, an increase of 1.8 per cent from October 2022. The average MLS residential price in BC was $968,786 up 4.1 per cent compared to October 2022. “However, the inventory of homes for sale remains quite low, despite a modest uptick in new listings. Consequently, markets have found balance, though at a very low level of activity.”

Around the Province

Major Point: Market is up when measured against 2022. But well down over previous years. See below.

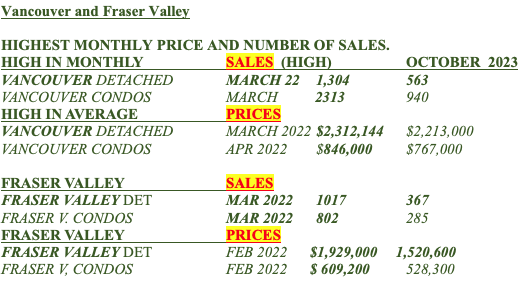

Snapshot October 2023 VANCOUVER AND FRASER VALLEY

We told you last year that, as we compare ourselves in 2023 to the same months in 2022, we will look great! The market collapsed last year – now it has recovered? Yes – somewhat.

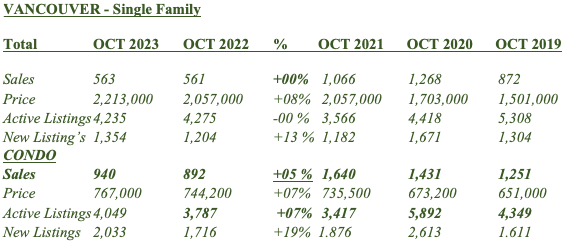

VANCOUVER

While SF sales are a tad better, they are still below 32% of the 10-year average for October. In fact in October 2023 we sold 563 SF homes. In 2021 we sold 1,066.

Vancouver SF new listings are up 13%. Condominium new listings are up 19%.

Here is a 5-year OCTOBER 2023 over OCTOBER 2022/2021/2020/2019 comparison.

- Major Point: SF sales are 563 up a tad over 2022 (561). Still sharply lower than 2021 (1,066)

- Vancouver prices best OCTOBER in last 4 years!

- (But still behind highest monthly prices achieved in last 4 years (see FV above)

- Talked to ACE Fraser Valley Realtor Brent Roberts. He says people write (low) offers but putting them together into a deal is a lot harder.

Get your professional realtor give you the numbers for the sub-area that YOU are interested in.

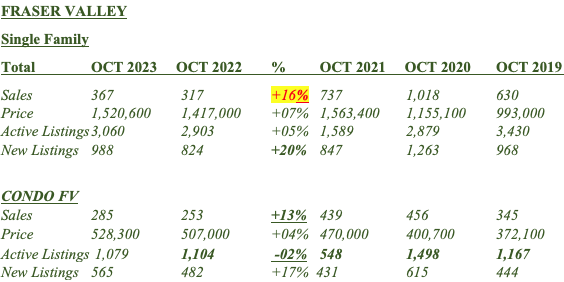

Major Point: Fraser Valley – SF Sales are up 16% over 2022. Still we are 47%+ lower than 2021 AND 67% lower than 2020.

New listings – are up 17% in condos; also up 20% in SF homes. We said last month: BUT now…

MAJOR, MAJOR POINT:

NOTE: Now we see market sales and prices reversing to ‘sideways’ even ‘lower.’ Rates could increase December 6 in Canada, a week later in US. Not likely but could.

WANT TO PARTICIPATE?

Go to www.realestatetalks.com – Some 2,500 members (47,009 posts) talk real estate. Ozzie created this bulletin board in 1998!

If you are in a real estate related industry of any sort (realtor, appraiser, lawyer, home inspector, etc.) list yourself in Ozzie’s free British Columbia real estate directory at www.bcred.ca.

OZZIE’S YOUTUBE CHANNEL

You can watch all videos and podcasts on my YouTube channel at https://www.youtube.com/jurockvideo. It is a great way to check on what I said 10 years ago.

Moneytalks Podcast

Ozzie, Michael Campbell, Michael Levy and Victor Adair and guests are now on podcasts every week: https://omny.fm/shows/money-talks-with-michael-campbell (See Victor Adair’s Trading Desk notes! https://victoradair.ca/)

OZBUZZ.CA

Why subscribe if I can just go to the website at Ozbuzz.ca? Hot properties and the latest podcasts are DISTRIBUTED TO SUBSCRIBERS FIRST– posted 2 weeks later on website.

HAVE A QUESTION OR COMMENT?

You can reach me at info@ozbuzz.ca with all of your questions, comments and concerns regarding the Oz Buzz publication.

Subscribe

| Subscribe to Oz Buzz: |

(You’ll get Oz Buzz 2 weeks before it’s posted online)

Oz Buzz Podcast

Disclaimer

Product Special

RECENT POSTS

Oz Buzz #97: All New Multiplex Changes Are Now Law

July 14, 2024 “The past is a great place, and I don’t want to erase it or regret it, but I don’t want

MORE URGENT! The new Multiplex! Where – how exactly? What rules? Get FREE STUDY – DEFINITIONS – CHECKLIST

Expert Guest: Bill Laidler, President of Laidler Academy and Laidler Development. Laidler is a trusted Real Estate Agent turned Multi-Family Developer in

Re Air BnB

Often bylaws disallow short term rentals in residential neighbourhoods.

Extra parking is one concern.

Also, nitely rentals of rental suites ate a real No-No!

They are an important component for employee accommodation. For example, in Whistler, where we require lots of bodies to fill all the low paying resort jobs( number in the thousands)