June 24, 2024

“I am no longer accepting the things I cannot change. I am changing the things I cannot accept.” –Angela Davis

NEW VIDEOS

Christian Dy and Ozzie discuss: “Capital Gains tax, crazy world…what actions you must take now!

Bill Laidler and Ozzie discuss: “3 Steps to Developing a Profitable Multiplex.”

John Weston (MP) and Ozzie: Incredible Game-Changer! Canadian Health and Fitness Bold Plan to Transform the Nation’s Health!

The above videos are also available as podcasts here:

Listen to Ozzie’s Podcast on OZCAST at www.ozbuzz.ca

Also on Apple cast, Amazon video, Spotify.

MARC JUROCK ‘S latest (Ad)ventures in THAILAND. You heard me! Yes! THAILAND.

Marc is back in town from Thailand, he’s glad to share his rich expertise in real estate investing, retirement planning, and running businesses in Southeast Asia. Marc lives in Thailand, operates an auberge hotel/hostel in Pattaya for the last 2 years and is well versed in all things Thailand.

He’s also on A NEW mission to help men break free from their routines, rediscover their true selves and live fully through his Project Dude Alive Thailand tours.

The next tour kicks off on September 9th—a 10-day, nearly all-inclusive adventure departing from YVR! The ultimate road trip! Only $3888 including flight!

Don’t miss this opportunity to Arrive, Revive, and Thrive!

Ready to embark on this life-changing journey? This will Sell Out so write him at marc@jurock.com now!

AGENDA

- WORLD INTEREST RATES IMPACT

- CANADA/US INTEREST RATES UP OR DOWN FROM HERE

- CANADA NUMBERS AND OUTLOOK

- INFLATION IS FOR REAL AND CONTINUING WITH A RECESSION IN BETWEEN

- INFLATION PUDDING

- WONDERING ABOUT RETIRING IN THAILAND, OR?

- ECONOMY – OUTLOOK

- THE FREE BOOK DEBACLE

- QUESTIONS, QUESTIONS

COMMENT

The free book debacle.

- Lots and lots – “did I say: Lots?” – of comments on the free book offer.

No, I did not benefit financially from offering the book. In fact, it was a cost to me. Yes, it was more difficult to download than I had been led to believe. No, you were able to download it to your phone or gadget or read it in Kindle…No, you did not have to download in Kindle. If! If you went to Amazon.ca.

- In many speeches I get blank stares when I mention anything AI, whether it is ChatGPT, Pictory etc., etc. I thought the book was well written as an entry point into AI and it was OFFERED free …a public service for members of Ozbuzz.

- Since the debacle I have had 9 authors offering to do the same thing for me. Eeeehmmm, weeeell…NO!

THE INFLATION PUDDING

PUDDING? EH, WELL HERE IS THE ‘PROOF IN THE PROVERBIAL

INFLATION PUDDING’

From the Kobeissi letter: True US Inflation Since January 2021 (CANADA IS WORSE)

- Eggs: 49.3%

- Gasoline: 47.8%

- Airfare: 32.7%

- Electricity: 29.3%

- Natural Gas: 26.9%

- Chicken: 23.9%

- Public Transportation: 22.2%

- Used Cars: 20.9%

- Milk: 15.0% 1

- Clothes: 13.5%

Over the last 3 years, the purchasing power of a US Dollar has declined by 16%.

Furthermore, over the last 5 years, the purchasing power of a US Dollar has declined by 23%.

This effectively means uninvested money from 2019 is now worth almost ONE FOURTH LESS today.

Kobeissi argues? “How is this a strong economy? As we stated in 2020, inflation has become the biggest involuntary tax of all time. Over $4 trillion of stimulus is costing us much more than that now and in the future. All as deficit spending crushes records.” Follow on Twitter to: @KobeissiLetter

Major Point: In over 600 newsletters, 4 authored books, 7 quoted bestsellers and countless speeches I pointed out as early as 1998 that we live in the world’s most unreported inflation of all time. Difference between then and now? It’s reported now and it continues unabated (always wanted to use that word).

INTEREST RATES: QUESTIONS ABOUND

Europe: The Swiss National Bank caught EVERYONE off guard, cutting rates for the second time this year. That sent the Swiss franc lower against the dollar. But not other European currencies . The Bank of England held its key rate unchanged, as did Norway’s Norges Bank. When you look at all central banks in the world and what their stance is on rates – you realize that NO ONE KNOWS!

Knows what? What to do. Call it unchartered waters. When you look at the bond markets, the key rates, the killing of negative rate experiments and the massive increase in debts. It is clear: WE WILL HAVE A RUNAWAY INFLATION. Of course: we also WILL HAVE A DEEP AND LASTING DEPRESSION.

The different views are not surprising, but who shared/holds them…is! Sorry, dear Reader, I don’t have the definitive answer either. But I direct you to my stance of early 2022. The High is in place and Cash is NOT trash! How much cash? As discussed before. Age related cash and market related cash. Over 70 – have 70 percent of your assets in cash or near cash. Under 40 ? Go for the brass ring, you can make it back! More views:

We said last months: Canada and the US are on divergent paths. For the US, it will stay higher longer. One reduction July/Sept.

Since then Canada (after higher for 4 years) reduced overnight rate by .25% while the US stayed pat – as forecast. Banks lowered their prime rate too… Now the big question is …choosing between variable and fixed rates. What to do?

As you know, variable mortgage rates will be affected by the Bank of Canada’s move. Those with a variable mortgage (about $14 per $100,000) and/or a Home Equity Line of Credit (about $21 per $100,000), will be positively impacted.

Fixed rates are following the bond rates. Now to see how fixed rates react! Bond yields have dropped to March lows, now to see if they hit Jan lows!

The central bank is scheduled to meet four more times before the end of 2024, with its next decision to arrive on July 24.

WHAT’S BETTER VARIABLE OR FIXED? Markets are now fully pricing in further rate cuts in September and December (.25% each) right on time for the bulk of those facing mortgage renewals — most of which are due in 2025 and 2026.

MOST IMPORTANTLY: Shop, shop till you drop for best rate. Worst rate is .75 bps above the lowest advertised rate.

ECONOMY: According to most sober forecasts, the economy is about to hit a rough patch, with rising unemployment, sluggish GDP growth, continued painful mortgage renewals and surging defaults (although not the catastrophic Global Financial Crisis-style defaults some see ahead). All this should be enough to accelerate the downward momentum in rates.

COMMENTS

Lots of comments on the capital gain (pending) new law. ALL of them very positive on our content. One echoed comment: “First time I understood it, my options and what I should do.” Ok, says Ozzie, as long as you check and check and check your options with YOUR tax lawyer and YOUR tax accountant.!

COMMENT: Surprising number of comments on the “bank calculators misleading”.

One specific good general comment I agree with: “It sems in today’s world, everything is about attention grabbing. Google a trip to Europe, get peppered by a hundred travel agencies. Google one SUV, every manufacturer gets your info and hammers you with theirs. Unasked for continuous email crowds out your regular email and then often if you get sucked in and do respond…nothing you actually asked for is answered, rather you are tricked into this or that advertisers’ corner.”

COMMENT:

C: Keep your opinions to yourself. You obviously do not understand the word tolerance. You just display your ignorance!

A: Hah ha ha ha ha ha. My blog is ENTIRELY PERSONAL OPINION! Your message speaks for itself.

The Tolerance piece raised a MANY heckles, more than my real estate comments. That razes me.

Dear guys/gals…If you are not worried how about how the WEST is the most desired place to be in by the whole world and how the West is becoming overrun by the wrong kind of immigration, its values challenged and abridged, you are a fool. Your tolerance is going to kill your honorable children and get them to run away to …? The East? Or with Ann Rynd architects?

COMMENTS: Got more and more stuff on EVs. All negative. Please send me some positive comments about owning one. Please, please…

COMMENT: Alberta tax comparison raised some astonishment and (some) outrage,

QUESTIONS, QUESTIONS

Several questions/comments on my offbeat notes: “Because we let them?”

Q: How and why do we let them?

A: We don’t fight for what we believe, we stay quiet, we scare of being cancelled. Yep, we let them!

Q: What is ESG? Should I make investment decision based on companies that proport to have focus on this.

A: I get this question often. So what is it? ESG investing incorporates environmental (E), social (S), and governance (G) considerations into investment decisions. According to the Fraser Institute:”… empirical studies, on balance, find no consistent and statistically significant evidence of a positive relationship between the ESG rankings of individual companies or portfolios of companies and the financial performances of those companies or investment portfolios.”

OZZIE HAS DARK THOUGHTS … ARISING FROM THIS COMMENT/QUESTION

Q: Ozzie, you always advise to spend an afternoon watching opposing views on YouTube shows. Dozens of experts watching the same statistics and then coming to opposing CONCLUSIONS AND PREDICTIONS. Well, I did one better, I actually took a weekday off. Weekends are for family. I then only watched positive forecasts in the morning (lower rates, higher stocks, rising real estate, no recession etc.). Then I had lunch. I felt good having watched such fine forecasters, giants of industry as they were so upbeat.

After lunch I watch 3 hours of recession, depression, soaring rates stock markets crashing…and unbelievably – as you forecast – they quoted the same or similar stats as the basis for their beliefs.

I noted they had something in common though. They all said – such and such will happen – unless there is a black swan.

You have often quoted Taleb (the originator of the book/concept.)

Now I tell you, I wish I hadn’t done the watching, I should have picked one or the other…I am totally confused. I am worried and happy except for the pending SWAN. So, I ask you: “WHAT BLACK SWAN COULD HAPPEN IN THE MIDDLE OF ALL THESE FORECASTRS?”

OK, here goes… THE (Proverbial) BLACK SWAN

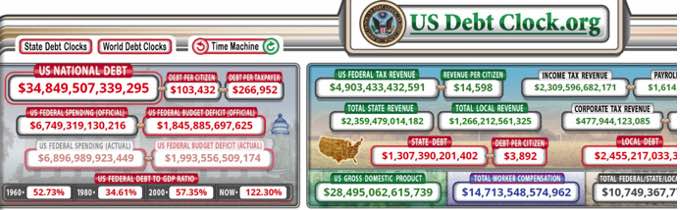

Asking me as to whither or what Black Swan, is getting a lot of interest, but no easy answer. By its nature a true Black Swan is a surprise. Anyway in my mind…the biggest and most likely unpopular Black Swan is clearly worldwide debt. The US national debt (look it up it changes constantly…is now approaching 35 Trillion. The world (depending on report) is between 326 to 600 Trillion. What of this debt could trigger a surprise Swan.

The Mortgage Bankers Association’s latest Commercial/Multifamily Mortgage Debt Outstanding quarterly report, the total commercial/multifamily mortgage debt outstanding rose to $4.70 trillion at the end of the first quarter. Multifamily mortgage debt alone increased $23.7 billion (1.1 percent) to $2.10 trillion from the fourth quarter of 2023.

Says Jamie Woodwell, MBA’s Head “Every major capital source increased its holdings of commercial mortgages, as fewer loans than usual were paid off through property sales or refinancings.

Who holds the debt? The four largest investor groups are: banks and thrifts; federal agency and government sponsored enterprise (GSE) portfolios and mortgage-backed securities (MBS); life insurance companies; and commercial mortgage-backed securities (CMBS), collateralized debt obligation (CDO) and other asset-backed securities (ABS) issues.

Commercial banks continue to hold the largest share (38 percent) of commercial/multifamily mortgages at $1.8 trillion. Agency and GSE portfolios and MBS are the second-largest holders of commercial/multifamily mortgages (22 percent) at $1.01 trillion. Life insurance companies hold $720 billion (15 percent), and CMBS, CDO and other ABS issues hold $604 billion (13 percent). Many life insurance companies, banks and the GSEs purchase and hold CMBS, CDO and other ABS issues. These loans appear in the report in the “CMBS, CDO and other ABS” category. (read the very detailed report and get a feel for the scope and size of the problem). Ask: Who holds most of the defaulting debt?

Looking solely at multifamily mortgages in the first quarter of 2024, agency and GSE portfolios and MBS hold the largest share of total multifamily debt outstanding at $1.01 billion (48 percent), followed by banks and thrifts with $620 billion (30 percent), life insurance companies with $230 billion (11 percent), state and local government with $117 billion (6 percent), and CMBS, CDO and other ABS issues holding $67 billion (3 percent).

It also is increasing!

Major Point: That is the Black Swan. All governments know it, all banks know it, all MBS holders know it. Likely outcome? Actually higher interest rates for longer? (Too much to dive in for our purpose… BUT the neutral rate — a theoretical level of flat borrowing costs that stays pat (no growth, no decline) — is much higher than policymakers want to see. Thus higher rates)

Unpleasant Solutions Black Swans?

- A major crash – wipe it all out (resurrect the Resolution Trust to help the clean up the wipe out)

- A major multinational war.

- The much touted ‘total reset’. And yes, I am not a conspiration fudger. But: The whole financial system based on how and what we pay is computerized, banks and governments will know every nickel you are spending and what taxes you are not paying. AI will take away most service jobs (although not nearly as fast as they tell us).

REAL ESTATE MARKETS CHANGING

LISTINGS UP EVERYWHERE – SALES LOWER

USA Housing starts and building permits fell from a month earlier, while weekly jobless claims, at 238,000, came in a bit higher than economists expected.

CANADA

It is interesting to note that as expensive as Canada’s real estate is, and as difficult it is to even rent, Royal Lepage reported in a survey that 27% of current tenants still want to buy as soon as possible. Even though some renters pay up to 50% of their income in rent!

Home sales in the Greater Toronto Area (GTA), Canada’s biggest housing market, declined 22% from a year earlier.

The Toronto Real Estate Board reported 7,013 sales in May, down from 8,960 that were sold in May 2023.New listings across the metropolitan region rose 21%, with 18,612 new properties put on the market during the month of May.

The MLS benchmark was down by 3.5 per cent in May 2024. The average selling price of $1,165,691 was down by 2.5 per cent over the May 2023 result of $1,195,409.

Anecdotally, we hear of increasing listings and lower sales to continue… Still waiting to see whether lower rates have a psychological impact. Active listings are up a whopping 84%.

LISTINGS UP EVERYWHERE except ALBERTA – DEFINITELY OPPORTUNITIES FOR BUYERS…

“If you put two economists in a room, you get two opinions, unless one of them is Lord Keynes, in which case you get three opinions.” – Winston Churchill

(This applies today!)

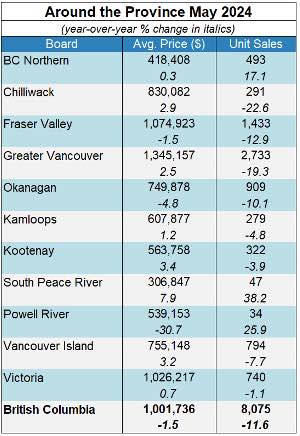

BRITISH COLUMBIA

BCREA reports 8,075 sales were in May 2024, a 12 per cent decrease from May 2023. The average price was down 1.5 per cent at $1 million. The total sales dollar volume was $8 billion, a 13 per cent decline from the same time the previous year.

BCREA : Source.

Sales ARE down 20% below 10-year average from TO and Vancouver.

Active listings (all things unsold at month end) are RISING in Vancouver 48%, in New Westminster up 78%, in Richmond 39%, in Coquitlam 60%.

VANCOUVER

SNAPSHOT MAY 2024 VANCOUVER AND FRASER VALLEY

As we compare ourselves in 2024 to the same months in 2023, we are seeing a further slowdown everywhere! We will be going through several valleys: The renewal valleys, the slowdown rallies, they harder to get approved valley etc., etc., but we WILL GET THRU THE VALLEYS.

Vancouver and Fraser Valley

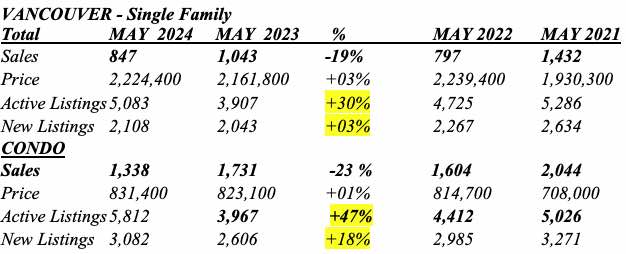

VANCOUVER

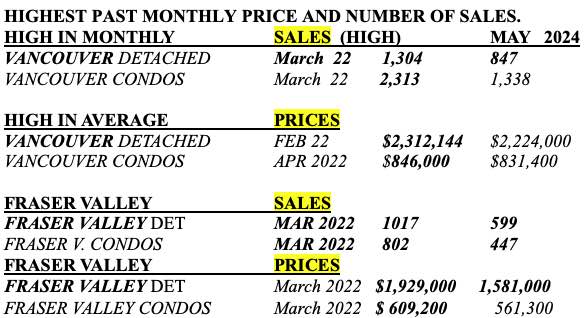

SF sales are still 20% well below the 10-year average for MAY. We remain way behind in number of properties sold! WAY behind! Look at the past.

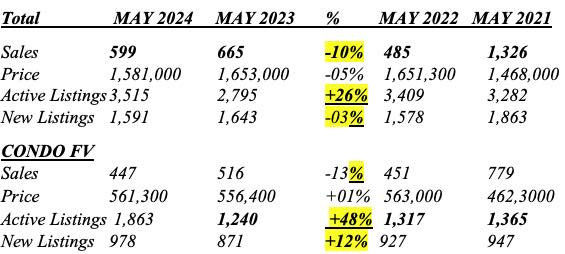

Here is a 4-year MAY 2024 over MAY 2023/2022/2021/ comparison.

- Major Point: SF sales remain dramatically below 2023 and 2021. Vancouver SF and condo prices about the same as 2023/2022!NOTE! New listings not as high as April (Condo and SF new listings in April rose at 60+%). Active listings (those unsold at end of May) are however much higher at 47%. (lower number of sales.

FRASER VALLEY – Single Family

Major Point: Fraser Valley – SF Sales were down again by 10% this month. Still 100+% lower than 2021 (1,326).

New listings are up ONLY 12% in condos; ACTUALLY DOWN 3% in SF homes. Active listings ARE up 26 % and 48% respectively! NOTE: Fewer new listings but rising active listings. Normal as there were fewer sales.

MAJOR, MAJOR POINT: The story in MAY was more SLOW DOWN – INCREASE IN PRODUCT. This will continue into June/July. Lots of anecdotal negatives in the Highrise Toronto real estate market.

RECENT POSTS

Oz Buzz #96: World Interest Rates Impact

June 24, 2024 “I am no longer accepting the things I cannot change. I am changing the things I cannot accept.” –Angela Davis

URGENT! 3 ways to profit from new Multiplex laws in BC. Pitfalls and massive opportunity if you know…

3 ways to profit from new Multiplex laws in BC. Pitfalls and massive opportunity if you know... Ozzie talks with Bill Laidler,

Leave A Comment